NFT Tax in Germany: How Crypto Tax Rules Apply to Your Digital Assets

Germany has one of the most distinctive approaches to crypto tax in Europe. For individual holders, the rules can actually work in your favour, but only if you understand them. At the heart of crypto tax Germany is a holding-period principle: dispose of a digital asset after more than twelve months and you pay no income tax on the gain, regardless of the amount. Sell within twelve months and the profit is taxed as miscellaneous income at your personal income tax rate. NFTs sit inside this same framework, but with a few extra layers worth understanding. Whether you bought a piece of generative art, a gaming item, or a collectible profile picture, the German tax authority, the Bundeszentralamt für Steuern and the wider Finanzamt network, treats the transaction as a private disposal under the Einkommensteuergesetz. This guide walks through how those rules apply in practice.

How Germany Classifies Crypto and NFT Gains

Germany does not treat cryptocurrency or NFTs as currency or as capital assets in the traditional sense. Instead, gains from disposing of these assets fall under Section 23 EStG as private sales transactions, specifically "sonstige Einkünfte" or miscellaneous income. This classification is important because it is what enables the twelve-month tax-free exemption that Germany is known for globally.

Tax Classification of Crypto and NFT Gains

For most individual filers, the classification means gains are added to your total income and taxed at your marginal rate, which can reach up to 45% for high earners, plus the solidarity surcharge. However, if you hold the asset for more than one year before selling, gifting, or otherwise disposing of it, the gain is completely exempt from tax. There is no reporting threshold to worry about beyond a minor annual free allowance for miscellaneous income overall.

NFTs are treated as "other economic goods" under this framework. The Bundeszentralamt für Steuern has not issued a standalone NFT-specific ruling as of the time of writing, but the existing guidance on crypto assets is broadly applied. An NFT is a unique token on a blockchain, and its disposal, whether by sale, swap, or even gifting at above-cost value, triggers a taxable event in the same way a fungible token would.

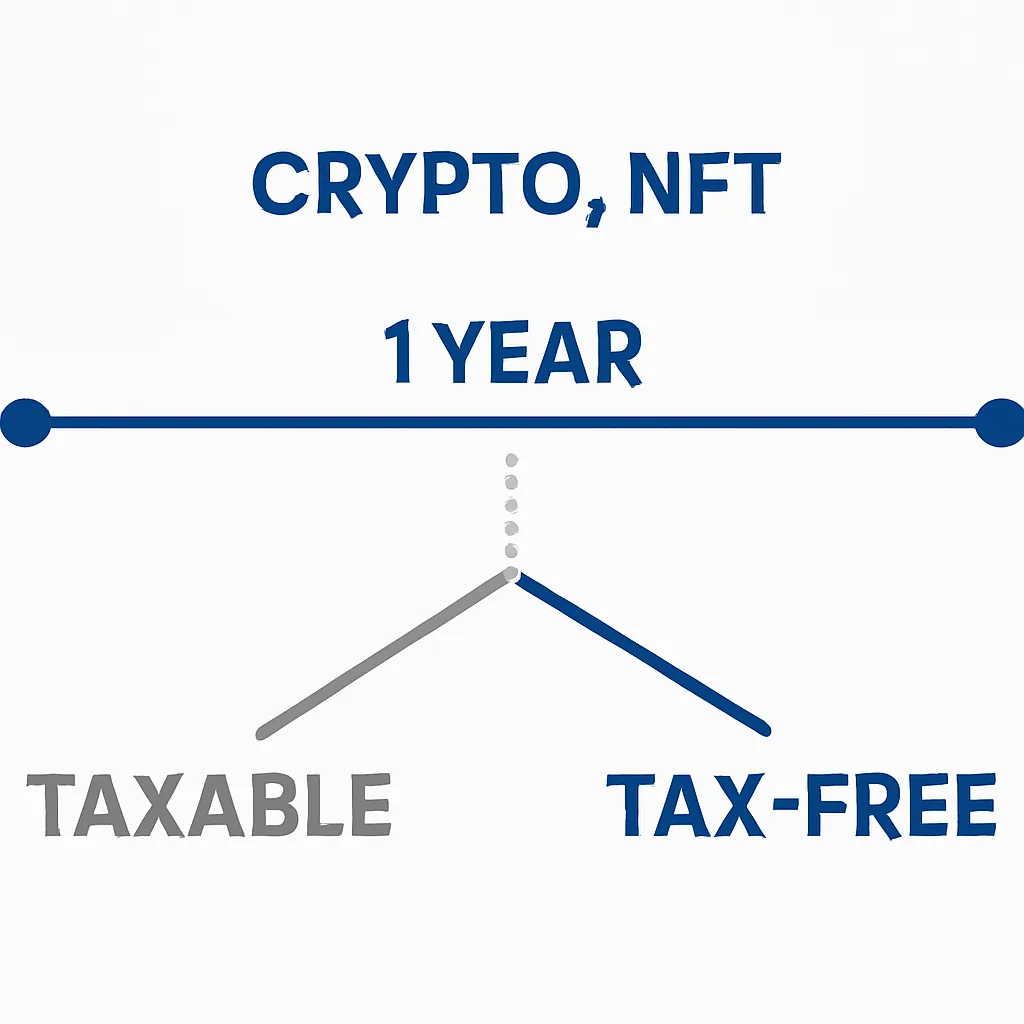

The One-Year Holding Period and Why It Matters for Crypto Tax Germany

The twelve-month exemption is the single most important feature of crypto tax Germany for private individuals. Buy an NFT or a coin in January and sell it in December of the same year, and any gain is taxable income. Hold until the following February and the same gain is entirely free of tax. This makes the purchase date one of the most valuable pieces of data you can record.

When the One-Year Rule Applies

The holding period starts on the date you acquired the asset, not the date you transferred it to a different wallet. Moving assets between your own wallets does not reset the clock. However, certain actions can restart the period or complicate the calculation. Using an NFT as collateral in a DeFi protocol, for example, may be treated as a disposal in some interpretations, though official German guidance on DeFi remains an evolving area.

For NFTs specifically, the one-year rule applies per token, since each NFT is a distinct asset with its own acquisition date and cost basis. If you hold a collection of ten NFTs purchased at different times, each one has its own holding clock running independently. This is very different from fungible tokens, where you pool acquisitions and apply a cost basis method such as FIFO.

Cost Basis and Record-Keeping for NFT Transactions

Calculating your gain requires knowing what you originally paid, your cost basis. For NFTs, this includes the purchase price of the token itself plus any transaction fees paid in ETH or another gas token at the time of purchase. Those fees are part of the acquisition cost and reduce your eventual taxable gain.

Cost Basis Calculation for NFTs

Germany applies the FIFO, first-in first-out, method as the default for fungible cryptocurrencies. For NFTs, which are unique by definition, cost basis is calculated on a per-token basis rather than pooled. You identify exactly which token you are selling and match it against its specific purchase cost. This sounds straightforward, but complications arise when the NFT was acquired through minting, where you paid gas fees but no explicit purchase price, or when it was received as a prize or airdrop.

The table below summarises how different NFT acquisition types affect the cost basis calculation under German tax principles.

Acquisition Methods and Cost Basis

| Acquisition Method | Cost Basis Approach | Notes |

|---|---|---|

| Market purchase (ETH/fiat) | Purchase price plus gas fees at acquisition | Most straightforward case |

| Mint | Mint price plus gas fees | If free mint, cost basis equals gas fees only |

| Received as gift | Fair market value at date of receipt | Holding period may carry over from donor in some interpretations |

| Airdrop or prize | Fair market value at date of receipt; receipt itself may be taxable | Consult a Steuerberater for airdrop-specific treatment |

| Swap for another NFT | Fair market value of asset given up at time of swap | Both sides of the swap may trigger a disposal event |

Staking, Royalties, and Income-Type Events

Not every crypto or NFT-related receipt is a capital gain question. Some events generate income rather than a disposal gain, and Germany taxes these differently. Creator royalties earned each time your NFT is resold on a secondary market are generally treated as income from a commercial activity if you are producing NFTs regularly. For a one-off creator, the treatment may fall under miscellaneous income instead. The distinction matters because commercial income attracts trade tax in addition to income tax.

Tax Treatment of Staking Rewards

Staking rewards for validators or liquidity providers are treated as income at the point of receipt, valued at the fair market price on the day they are credited. A separate question then arises when you later dispose of those staking rewards: the holding period for the received tokens starts from the date they were credited to you, not from any earlier date.

NFT-related income such as licensing fees, play-to-earn game rewards, or fractional ownership distributions each carry their own classification questions. Germany's tax framework is principles-based in this area, meaning you apply the general income tax rules to each specific fact pattern rather than looking up a single definitive answer. Keeping detailed records of every receipt, including its euro value on the day, is essential.

How Crypto Tax Rules Compare Across Germany, the UK, and India

Germany's approach stands out internationally because of the long-term exemption. Comparing it with two other major jurisdictions helps illustrate why the holding period matters so much and why filers in different countries face very different obligations. Understanding how is crypto taxed in Germany versus other regimes is a common question for internationally mobile individuals.

International Comparison of Crypto Tax Rules

| Jurisdiction | Tax on Short-Term Gains | Tax on Long-Term Gains | NFT Treatment | Key Feature |

|---|---|---|---|---|

| Germany | Marginal income tax rate (up to ~45%) | 0% after 12 months | Same as other private disposal assets | 12-month exemption is unique in Europe |

| United Kingdom | Capital gains tax at 18% or 24% depending on total income | Same CGT rates apply; no time-based exemption | Treated as a capital asset by HMRC | Annual CGT allowance (check current year figure with HMRC) |

| India | Flat 30% on VDA gains regardless of holding period | Same 30% flat rate applies | Classified as Virtual Digital Asset under Finance Act 2022 | No deductions except cost of acquisition; 1% TDS on transfers |

For UK-based holders, crypto tax UK rules mean every disposal is a capital event with no time-based exemption, making a germany crypto tax calculator or an India-focused tool unsuitable. For Indian filers, the flat 30% rate and the 1% tax deducted at source on transactions make record-keeping equally critical. If you use a crypto tax calculator, always confirm it is configured for your specific jurisdiction.

Common Mistakes German NFT Holders Make at Tax Time

One of the most frequent errors is failing to record the euro value of an NFT at the exact moment of purchase. Because NFTs are usually priced and transacted in ETH or another crypto asset, you need to convert the price to euros using the exchange rate on the transaction date. Leaving this step until the end of the tax year, when historical rates can be harder to retrieve accurately, creates unnecessary risk.

Common Tax Mistakes for NFT Holders

A second common mistake is treating a wallet-to-wallet transfer as a non-event without checking whether the receiving wallet is genuinely still under your sole control. If you send an NFT to a friend's wallet as a gift, that is a disposal at fair market value, even if no cash changes hands. The gain is measured against your original cost basis.

A third area of confusion involves NFT swaps on platforms that allow direct token-for-token trades. Each side of the swap is a separate disposal event. You have disposed of what you gave and acquired what you received, both at fair market value at the time of the trade. This can create two taxable events from a single transaction that felt like a simple exchange.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Lena is a graphic designer based in Berlin who began collecting digital art NFTs as a hobby in early 2022. She purchased three NFTs over the course of the year using ETH, carefully recording the ETH price in euros on each transaction date. By spring 2024, two of those NFTs had appreciated significantly. Because she had held both for more than twelve months, she sold them without owing any income tax on the gains under the Section 23 EStG exemption. The third NFT, acquired just eight months before she sold it, generated a gain that was fully taxable at her marginal rate.

Lena used CryptaTax to upload her wallet transaction history, which automatically calculated the holding period for each token, converted historical ETH prices to euros, and flagged the one short-term disposal requiring declaration. Her Steuerberater received a clean, ready-to-file summary. The process that had seemed overwhelming when she first considered her obligations turned out to be manageable once the data was organised correctly.

Frequently Asked Questions

Do I have to pay crypto tax in Germany if I held for more than one year?

If you held the asset for more than twelve months before disposing of it, the gain is exempt from income tax under Section 23 EStG for private individuals. This applies to both fungible cryptocurrencies and NFTs. You still need to be able to demonstrate the holding period with accurate records if the Finanzamt asks.

How is crypto taxed in Germany if I sell within twelve months?

Any gain realised within twelve months of acquisition is treated as miscellaneous income and taxed at your personal marginal income tax rate, which can reach up to 45% plus the solidarity surcharge. Losses from short-term disposals can be offset against gains in the same category within the same tax year.

Are NFTs treated differently from Bitcoin or ETH for German tax purposes?

NFTs are classified as other economic goods under German tax law rather than as currency or capital assets. However, the same private disposal rules under Section 23 EStG apply, including the twelve-month exemption. The main practical difference is that each NFT has its own individual cost basis and holding period, unlike fungible tokens where FIFO pooling applies.

What counts as a taxable event for NFTs in Germany?

Selling an NFT for fiat or crypto, swapping one NFT for another, gifting an NFT at above-cost value, and using an NFT as collateral in certain DeFi protocols can all constitute taxable disposal events. Receiving an NFT as a gift or airdrop may itself create an income event at fair market value on the date of receipt.

Do I need a germany crypto tax calculator to file correctly?

You are not legally required to use specific software, but given the complexity of tracking acquisition dates, euro conversion rates, gas fees, and individual NFT cost bases across multiple wallets, a dedicated germany crypto tax calculator reduces the risk of errors. Manual spreadsheet tracking is possible for simple portfolios but becomes difficult to audit as transaction volumes grow.

How does crypto tax in Germany compare to crypto tax in the UK?

Germany's twelve-month tax-free exemption has no equivalent in the UK. Under crypto tax UK rules, all gains are subject to capital gains tax regardless of holding period, though an annual CGT allowance may reduce the bill. Rates and allowances differ significantly, so a tool or adviser specific to your country of residence is essential.

How is crypto taxed in India compared to Germany?

India applies a flat 30% tax on gains from Virtual Digital Assets including crypto and NFTs, with no time-based exemption and no ability to deduct expenses other than the original acquisition cost. Germany by contrast allows the twelve-month exemption and deduction of transaction fees. An India crypto tax calculator will apply completely different rules from a German one, so jurisdiction matters enormously.

What records should I keep for my NFT transactions in Germany?

You should keep the acquisition date, the purchase price in the token used, the euro equivalent at the exact transaction date, all gas fees paid in connection with the purchase and sale, the wallet addresses involved, and the disposal date and proceeds. The Finanzamt can request substantiation for up to ten years, so durable record storage matters.

What happens if I made a loss on an NFT sale in Germany?

Losses from NFT or crypto disposals within the twelve-month window can be offset against gains in the same miscellaneous income category in the same tax year. They cannot be offset against salary, rental income, or other income categories. Unused losses in this category can be carried forward to future years, though they remain ring-fenced.

Does the twelve-month exemption still apply if I used my NFT for staking or DeFi?

This is an unsettled area. Some tax advisers argue that using a crypto asset to generate income, such as through staking or liquidity provision, extends the holding period required for tax exemption from twelve months to ten years under Section 23 EStG. Others contest this interpretation for NFTs specifically. If you have used NFTs in yield-generating protocols, consult a qualified Steuerberater before assuming the standard twelve-month rule applies.

Source: CryptaTax