Crypto Tax Germany: A Complete Guide for Individuals

Crypto tax in Germany works very differently from most other major jurisdictions, and that difference can work heavily in your favour if you plan ahead. Germany treats cryptocurrency as a private asset rather than a financial instrument, which means the rules that apply to you as an individual are rooted in income tax law rather than capital gains tax. The headline benefit is well known: hold your crypto for more than one year and any profit you make is entirely tax-free. No tax on disposal, no tax on conversion, no reporting obligation on gains. That one rule alone shapes almost every decision a German crypto investor needs to make. But the framework has layers. Staking, lending, mining, and short-term trading all carry their own treatments, and getting them wrong can be costly. This guide covers everything you need to know, including how Germany compares to the crypto tax rules in India and the UK for anyone who has tax obligations in more than one country.

How Is Crypto Taxed in Germany: The Core Framework

Germany classifies cryptocurrency, including Bitcoin and Ether, as a Wirtschaftsgut, a private economic asset, under Section 23 of the Einkommensteuergesetz, the German Income Tax Act. This classification is central to understanding how is crypto taxed in Germany. When you sell, swap, or otherwise dispose of a private asset within one year of acquiring it, any profit is taxable as a private disposal gain. The gain is added to your other income for the year and taxed at your personal income tax rate, which ranges from the basic rate up to the top rate, plus the solidarity surcharge where applicable. If your total private disposal gains for a tax year fall below a small annual threshold, no tax is due at all, though you should still track your positions carefully because this exemption applies to all private disposal assets combined, not just crypto. Losses from short-term crypto disposals can be offset against gains from other private disposal transactions in the same year, or carried forward to reduce gains in future years. They cannot, however, be offset against employment income or other categories of income. The discipline required here is precise record-keeping from day one.

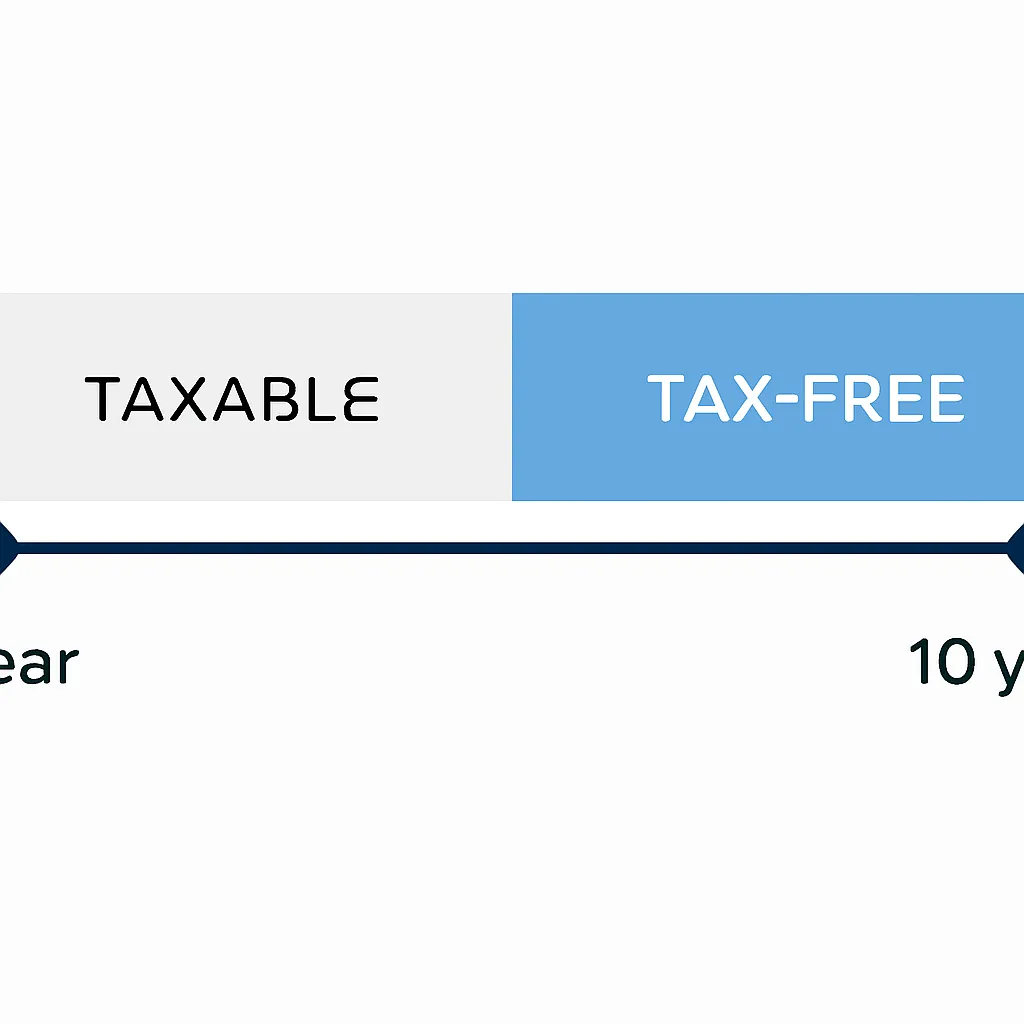

The One-Year Holding Rule and the Ten-Year Extension

The one-year holding period is the most powerful tool available to German crypto investors. Any asset held for more than 365 days before disposal is treated as a long-term private asset, and the gain is fully exempt from income tax regardless of its size. There is no cap, no taper, and no partial relief. The exemption is binary: you either qualify or you do not, and the cut-off is the calendar day of acquisition. Cost basis is calculated using the first-in, first-out method by default, meaning your oldest coins are deemed sold first. This matters enormously when you have bought the same asset at multiple points in time and want to make a selective disposal. There is one important extension to be aware of. Where crypto is used to generate income, for example through staking rewards credited to a wallet or through lending arrangements that produce interest-like returns, some tax practitioners and the German Federal Ministry of Finance have indicated that the holding period relevant to the original staked or lent asset may extend to ten years before the tax-free exemption applies. This interpretation is still debated and has not been settled definitively by legislation, so anyone with significant staking positions should take qualified advice before assuming a straight one-year rule applies to those specific coins.

Staking, Mining, and DeFi: Where the Tax Gets Complicated

Passive income from crypto is taxed differently from disposal gains in Germany. Staking rewards, mining income, and interest from crypto lending arrangements are generally treated as miscellaneous income under Section 22 of the Income Tax Act. This income is taxable in the year it is received, at your marginal income tax rate. A separate annual allowance applies specifically to this miscellaneous income category, and gains below that threshold are not subject to tax, though the threshold is modest. Mining is treated similarly but with an additional consideration: if mining activity reaches a commercial scale, it may be reclassified as a trade, which brings business income rules, VAT considerations, and the possibility of trade tax into play. For most individuals running a small mining operation or staking a modest amount of ETH, the miscellaneous income route applies. DeFi is the most unsettled area. Liquidity provision, yield farming, and wrapped token mechanics do not map cleanly onto the existing private asset framework. The German tax authorities have not issued comprehensive guidance on these transactions, and practitioners are applying first-principles analysis case by case. If you are active in DeFi, document every transaction, including the value at the time of each swap or deposit, because the lack of clear rules does not mean the lack of a tax charge.

Tax Treatment of Passive Income

| Transaction Type | Tax Treatment in Germany | Relevant Rate |

|---|---|---|

| Disposal within one year of acquisition | Taxable private disposal gain | Personal income tax rate |

| Disposal after one year of acquisition | Tax-free | 0% |

| Staking rewards received | Miscellaneous income, taxable on receipt | Personal income tax rate |

| Mining income (non-commercial) | Miscellaneous income | Personal income tax rate |

| Crypto-to-crypto swap within one year | Taxable disposal event, gain or loss crystallised | Personal income tax rate |

| Crypto received as payment for services | Taxable income at fair market value on receipt | Personal income tax rate |

Germany Crypto Tax Calculator: How to Work Out What You Owe

Calculating your crypto tax liability manually in Germany is possible but time-consuming once you move beyond a handful of transactions. The core calculation follows three steps. First, identify every disposal event during the tax year, which includes sales for euros or other fiat, swaps between crypto assets, and spending crypto on goods or services. Second, match each disposal to its acquisition using first-in, first-out, establish the acquisition cost in euros at the time of purchase, and subtract it from the proceeds in euros at the time of disposal. Third, sum all taxable gains and losses, apply the annual private disposal exemption if your net gains fall below it, and apply your income tax rate to any remaining taxable amount. A germany crypto tax calculator automates this process by connecting to exchange APIs or accepting transaction history exports, applying FIFO across your full portfolio, identifying which holdings have passed the one-year threshold, and producing a pre-filled summary ready for your tax return. When choosing a calculator, check whether it handles the ten-year staking holding period question, whether it supports the exchanges and wallets you use, and whether it exports in a format compatible with the German tax filing system. CryptaTax connects to all major exchanges, applies FIFO automatically, and flags positions approaching the one-year holding threshold so you can make informed decisions before year-end.

How Germany Compares to Crypto Tax in India and the UK

For individuals with connections to more than one country, understanding how the German approach differs from other major frameworks is essential. Crypto tax in India operates under a completely separate regime introduced in 2022. India imposes a flat rate on gains from virtual digital assets with no offset permitted for losses from one asset against gains from another. Expenses other than the cost of acquisition are not deductible. There is also a tax deducted at source on transfers above a certain value, creating a withholding mechanism at the point of transaction. An india crypto tax calculator needs to handle TDS credits, the flat rate calculation, and the strict loss ring-fencing rules, which are all fundamentally different from the German private asset framework. Crypto tax in the UK sits somewhere between the two. HMRC treats crypto as a capital asset, taxing gains at capital gains tax rates, which differ from income tax rates, with an annual exempt amount available. The UK uses a specific pooling method called the Section 104 pool combined with same-day and bed-and-breakfast matching rules, rather than FIFO. Unlike Germany, the UK offers no blanket exemption based on a holding period. The table below summarises the key structural differences.

Comparison of Crypto Tax Frameworks

| Feature | Germany | India | UK |

|---|---|---|---|

| Asset classification | Private economic asset | Virtual digital asset | Capital asset |

| Holding period exemption | Tax-free after one year | None | None |

| Tax rate on short-term gains | Personal income tax rate | Flat rate (no offset) | Capital gains tax rate |

| Loss offsetting | Against same-category gains | Not permitted across assets | Against capital gains |

| Cost basis method | FIFO | Cost of acquisition | Section 104 pool with matching rules |

| Staking income treatment | Miscellaneous income on receipt | Taxable as VDA gain | Income tax on receipt |

Filing Your Crypto Tax Return in Germany

German tax returns covering crypto transactions are filed through the ELSTER portal, the official online tax submission system. The relevant schedule for private disposal gains is Anlage SO. You report the total proceeds, total acquisition costs, and net gain or loss for each asset class, not each individual transaction, though you must be able to produce transaction-level detail if the tax office requests it. The German tax year runs on the calendar year, and returns are generally due by the end of July of the following year for self-filers, with an extension available if a tax adviser prepares the return. If you hold crypto across multiple exchanges and wallets, the practical challenge is aggregating your transaction history into a single coherent record before you can complete Anlage SO accurately. Crypto transactions on foreign exchanges are not automatically reported to the German tax authorities under current rules, but the Common Reporting Standard and the OECD's Crypto-Asset Reporting Framework are progressively closing that gap. EU member states including Germany will be required to implement CARF-equivalent reporting under DAC8, which will create automatic exchange of crypto account information between tax authorities across the EU. Filing accurately now, before automated reporting becomes standard, is both a legal obligation and a practical insurance policy against future scrutiny.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario: Lena is a freelance UX designer based in Berlin. She bought Bitcoin at various points over two years and also receives a modest amount of ETH each month as staking rewards through a delegated validator. In March of the current tax year she sold a portion of her Bitcoin holdings, some of which she had held for fourteen months and some for only eight months. The coins held for fourteen months are fully exempt. The coins held for eight months produce a taxable gain that she must report on Anlage SO. Her staking rewards are taxable as miscellaneous income in the year each reward was credited to her wallet, and she needs the euro value of each reward on the day it arrived. Lena uses CryptaTax to connect her exchange account and her staking wallet. The platform applies FIFO across her Bitcoin stack, separates the sub-one-year coins from the exempt long-term holdings automatically, imports her staking reward history with daily price data, and generates a completed Anlage SO summary. She reviews the output, confirms the figures, and exports the file for her Steuerberater to review before submission. The process takes her less than an hour rather than a weekend.

Frequently Asked Questions

Do I pay crypto tax in Germany if I only hold and never sell?

No. Simply holding cryptocurrency in Germany does not trigger any tax charge. Tax only arises when you dispose of an asset, which includes selling for fiat, swapping for another crypto, or spending it. Unrealised gains are never taxed under the current German private asset framework.

Is crypto tax in Germany really zero after one year?

For straightforward buy-and-sell transactions, yes. A private disposal of cryptocurrency held for more than one year is fully exempt from income tax under Section 23 of the German Income Tax Act. There is no cap on the exempt amount. The main caveat is the potential ten-year rule for assets that have been used to generate income through staking or lending, which remains a point of professional debate.

How is crypto taxed in Germany if I swap one coin for another?

A crypto-to-crypto swap is treated as a disposal of the asset you are giving up and an acquisition of the asset you are receiving. If you held the original asset for less than one year, any gain is taxable at your personal income tax rate. If you held it for more than one year, the disposal is tax-free regardless of the swap value.

What is the annual exemption for private disposal gains in Germany?

There is a small annual exemption threshold for private disposal gains, below which no tax is due. This threshold applies to all private disposal assets combined, not only crypto. If your net gains across all qualifying assets remain below this threshold for the year, you have no tax liability on those gains, though record-keeping obligations still apply.

How does the germany crypto tax calculator on CryptaTax work?

CryptaTax connects to your exchange accounts and wallets via API or CSV import, applies FIFO cost basis calculation across your full transaction history, identifies which disposals fall within or outside the one-year holding period, calculates taxable gains and miscellaneous income from staking, and generates a summary formatted for Anlage SO. It also flags holdings approaching the one-year threshold before you make disposal decisions.

How does crypto tax in India differ from Germany?

Crypto tax in India applies a flat tax rate on gains from virtual digital assets with no loss offsetting permitted between different assets. Germany by contrast taxes short-term gains at your personal rate, allows loss offsets against same-category gains, and exempts long-term gains entirely after one year. India also operates a tax deducted at source mechanism on crypto transfers above a specified threshold, which has no equivalent in Germany.

Is there a crypto tax calculator for India that works differently from a German one?

Yes. An india crypto tax calculator needs to handle the flat rate structure, the TDS credit reconciliation, and the strict prohibition on cross-asset loss offsetting, none of which apply in Germany. Using a calculator built for one jurisdiction to compute liability in another will produce incorrect results. CryptaTax supports multiple jurisdictions with country-specific rule sets applied automatically based on your tax residency settings.

How is crypto taxed in the UK compared to Germany?

Crypto tax in the UK falls under capital gains tax rather than income tax on private disposals. The UK has no holding-period exemption, uses the Section 104 pooling method with same-day and thirty-day matching rules, and taxes gains at capital gains tax rates rather than income tax rates. German residents who relocate to the UK should take specific advice on the interaction between the two systems, including any exit tax considerations on departure from Germany.

Do German crypto investors need to report transactions to the tax office even if they made a loss?

If your net private disposal result for the year is a loss, you should still report it on Anlage SO because the loss can be carried forward to offset gains in future years. Failing to report a loss means losing the benefit of the carry-forward. Gains below the annual exemption threshold do not legally require reporting, but maintaining records is strongly advisable given the trajectory of automatic information exchange under DAC8 and CARF.

What records should I keep for crypto tax in Germany?

You should retain the date and time of every acquisition and disposal, the euro value at the point of each transaction, the exchange or wallet involved, any transaction fees paid, and records of staking or mining income with the daily euro value on each receipt date. German tax authorities can request records going back several years, so cloud-backed exports from your exchanges and a reliable transaction log are both important. CryptaTax stores and organises this data automatically once connected to your accounts.

Source: CryptaTax