UK Section 104 Pool for Crypto: How to Calculate Your Tax Correctly

If you have bought and sold cryptocurrency in the UK, you cannot simply match each sale to the coin you paid the most for and call it a day. HMRC requires you to calculate gains using a specific pooling method called the Section 104 pool, and getting it wrong is one of the most common reasons crypto traders end up with an incorrect tax bill. A reliable crypto tax calculator will apply this method automatically, but understanding the underlying rules means you can check your figures, respond confidently to any HMRC enquiry, and file your self-assessment return without second-guessing every line. This guide explains exactly how the Section 104 pool works, when the same-day and 30-day rules override it, and what your final crypto tax report needs to show.

What Is the Section 104 Pool?

The Section 104 pool takes its name from Section 104 of the Taxation of Chargeable Gains Act 1992. HMRC applies the same legislation to cryptocurrency that was originally written for shares, treating each type of token you hold as a single, constantly updating pool of assets rather than a collection of individually identified coins.

How the Pool Updates

Every time you buy more of a particular token, two things happen to your pool: the total number of tokens increases, and the total allowable cost increases by the amount you paid, including any transaction fees HMRC allows. The pool therefore carries a running average cost per token. When you sell, you remove a proportion of that pool and calculate your gain against the corresponding slice of the pooled cost. You never ask which specific coins were sold. You ask what fraction of the pool was disposed of, and what that fraction cost on average.

This approach matters because crypto traders often buy the same token dozens of times at different prices. Without a pooling rule, traders could cherry-pick their highest-cost lots to minimise taxable gains. The Section 104 pool removes that flexibility and creates a consistent, auditable method that HMRC can verify.

The table below summarises the core mechanics of how the pool changes with each transaction.

| Event | Effect on Pool Quantity | Effect on Pool Cost |

|---|---|---|

| Purchase | Increases by units bought | Increases by total cost paid (including allowable fees) |

| Disposal (sale, swap, gift) | Decreases by units disposed of | Decreases by proportional share of pooled cost |

| Hard fork / airdrop receiving new token | New separate pool created at nil or market cost | Determined by HMRC guidance at time of receipt |

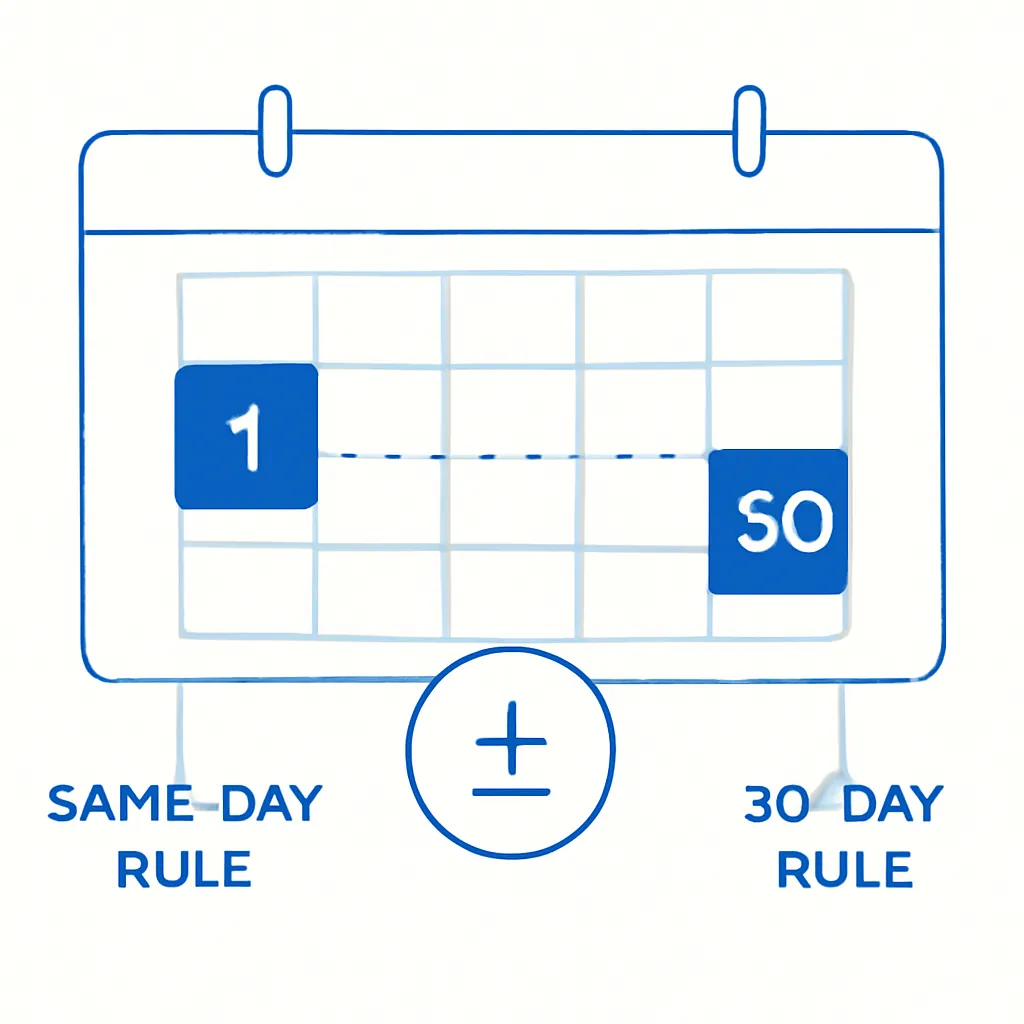

The Same-Day Rule and Why It Comes First

The Section 104 pool does not operate in isolation. HMRC applies a strict hierarchy of matching rules before any disposal falls into the pool, and the same-day rule sits at the top of that hierarchy. If you buy and sell the same token on the same day, HMRC matches those transactions against each other first. The pool is not touched for the matched portion.

Why the Same-Day Rule Exists

This rule exists to prevent a technique sometimes called bed-and-breakfasting, where a trader sells an asset to crystallise a loss and immediately buys it back, artificially refreshing their cost base. By matching same-day acquisitions first, HMRC closes the simplest version of that loop. The practical consequence for traders is that a large same-day purchase made shortly after a sale will be matched to that sale, not added to the pool, and the gain or loss on that disposal will be calculated using the cost of the same-day purchase rather than the pool average.

This can produce a significantly different result. If your pool average cost is lower than your same-day purchase price, the same-day match will reduce or eliminate a gain that the pool calculation alone might have generated. Getting the order of matching rules right is one of the most common areas where manual spreadsheets go wrong, and it is one of the clearest arguments for using dedicated crypto tax software that applies the rules automatically and in the correct sequence.

The 30-Day Bed-and-Breakfasting Rule

The second override in HMRC's matching hierarchy is the 30-day rule, which applies when you sell tokens and then buy the same type of token again within 30 days of that sale. In that case, the sale is matched against the subsequent acquisition rather than against the pool, and the gain or loss is calculated using the cost of the new purchase.

Why the 30-Day Rule Exists

The logic mirrors the same-day rule. If you could sell at a loss, crystallise that loss for tax purposes, and buy back within a matter of days, you would effectively manufacture deductible losses without any real economic change in your position. The 30-day window prevents this.

Traders who are actively rebalancing portfolios or deploying capital across market dips need to be especially careful here. A disposal made in late February could be matched to a purchase made in early March, overriding what would otherwise have been a pool-based calculation. When you calculate crypto taxes across a full tax year, every repurchase within 30 days of a disposal needs to be identified and matched before the remaining disposals are allocated to the Section 104 pool.

Matching Priority Order

The table below shows the correct order in which HMRC matches disposals.

| Matching Priority | Rule | Applies When |

|---|---|---|

| 1st | Same-day rule | Acquisition and disposal of same token on same day |

| 2nd | 30-day rule (bed-and-breakfasting) | Acquisition of same token within 30 days after disposal |

| 3rd | Section 104 pool | Any remaining unmatched disposal |

How to Calculate Your Section 104 Pool Gain Step by Step

Once you have applied the same-day and 30-day rules and confirmed that a disposal falls to the pool, the calculation itself follows a straightforward formula. You take the disposal proceeds, subtract the allowable cost drawn from the pool, and subtract any directly attributable transaction fees. The result is your chargeable gain or an allowable loss.

Calculating Allowable Pool Cost

The allowable cost drawn from the pool is calculated as follows: divide the number of tokens disposed of by the total tokens in the pool immediately before the disposal, then multiply that fraction by the total pooled cost. That figure is removed from the pool permanently.

For example, suppose your pool holds 5 ETH at a total pooled cost of £8,000, giving an average cost of £1,600 per ETH. You sell 2 ETH for £4,200 and pay a £20 transaction fee. The allowable pool cost for the disposal is 2 divided by 5 multiplied by £8,000, which equals £3,200. Your gain is £4,200 minus £3,200 minus £20, which is £980. After the disposal, your pool holds 3 ETH at a remaining pooled cost of £4,800.

Repeat for Every Disposal

This calculation has to be repeated for every disposal across the tax year before you can complete your crypto capital gains calculator output or prepare your crypto tax report for submission.

Which Transactions Count as Disposals?

A disposal is not limited to selling crypto for sterling. HMRC treats a wide range of events as disposals that trigger a Section 104 pool calculation. Swapping one token for another is a disposal of the token you give up. Spending crypto on goods or services is a disposal. Gifting crypto to anyone other than a spouse or civil partner is a disposal at market value. Moving crypto to a different wallet you own is not a disposal, but only if you can prove both wallets belong to you.

Income Events and Cost Base

Staking rewards and airdrops are generally treated as income at the point of receipt, which means the market value at receipt becomes the new cost base for those tokens when they are later disposed of. Each of those subsequent sales will feed into or draw from its own Section 104 pool for that token type.

Identifying All Disposal Events

Knowing how to file crypto taxes correctly means identifying every disposal event across every exchange and wallet you used during the tax year, not just the trades you made on a single platform. Many traders underestimate the number of taxable events in a given year, particularly if they have moved between wallets or used decentralised exchanges where no tax form is issued automatically.

Common Errors That Distort Your Pool Calculation

The most frequent mistake is ignoring the same-day and 30-day rules entirely and sending every transaction straight to the pool. This produces incorrect gain figures, usually understated losses or overstated gains, depending on the price movement between sale and repurchase.

Ignoring Same-Day and 30-Day Rules

A second common error is failing to include allowable fees in the pooled cost. HMRC permits transaction fees paid to acquire a token to be added to the pool cost. Overlooking these reduces your pool cost and inflates your gains unnecessarily.

Using the wrong exchange rate for non-sterling transactions is another pitfall. If you bought ETH with USDC on a foreign exchange, you still need to express both the cost and the proceeds in sterling at the appropriate exchange rate for the transaction date. Inconsistent rate sources across a tax year can produce a pool cost that is materially wrong.

Wrapped Token Confusion

Finally, treating wrapped tokens as identical to the underlying asset is a common but risky assumption. HMRC has not confirmed that wrapping is a non-disposal event in all circumstances, so mixing wrapped and unwrapped token quantities in the same pool can lead to errors that are difficult to unwind later.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Priya is a software developer based in London. She has been buying and selling ETH and BTC across three exchanges over two tax years and has never filed a crypto tax return. She knows she has made gains but has been putting off the calculation because she assumed she could simply use her average purchase price from one exchange's dashboard. A friend mentions the Section 104 pool rules, and Priya realises her approach has been wrong from the start.

She signs up for CryptaTax and connects her exchange accounts. The software imports her full transaction history, identifies four instances where the 30-day rule applies to ETH disposals she had previously sent straight to the pool, and recalculates her Section 104 pool for each token correctly. Her actual taxable gain turns out to be lower than her manual estimate because two of the 30-day matches happened at a higher cost than the pool average. CryptaTax generates a crypto tax report formatted for self-assessment, showing her total gains, losses, and the calculations behind each disposal. Priya submits her return before the January deadline with confidence rather than guesswork.

Frequently Asked Questions

What is the Section 104 pool for crypto in the UK?

The Section 104 pool is HMRC's default method for calculating gains on cryptocurrency disposals. It treats all tokens of the same type that you hold as a single pool with a running average cost. When you sell, the gain is calculated against a proportional share of that pooled cost rather than any specific purchase lot.

Do I need a crypto tax calculator to apply Section 104 pool rules?

You are not legally required to use software, but a crypto tax calculator makes the process significantly more accurate. The same-day rule, 30-day rule, and pool calculations all need to be applied in the correct order across every transaction in a tax year, which is extremely difficult to do reliably in a manual spreadsheet once you have more than a few dozen trades.

Does the Section 104 pool apply to every cryptocurrency?

Yes. HMRC applies the Section 104 pool to each token type individually. Your ETH pool is separate from your BTC pool, your SOL pool, and so on. Each pool has its own running quantity and cost, and disposals of one token type never affect the pool of another.

How do I calculate crypto taxes if I used multiple exchanges?

You must combine all transactions for the same token type across all exchanges into a single Section 104 pool. The exchange you used does not create a separate pool. You need to import your full transaction history from every platform and wallet before you can calculate crypto taxes accurately for the year.

What counts as a disposal for UK crypto capital gains?

A disposal includes selling crypto for fiat currency, swapping one token for another, spending crypto on goods or services, and gifting crypto to anyone other than your spouse or civil partner. Simply transferring crypto between your own wallets is not a disposal, provided you can demonstrate both wallets belong to you.

How does the 30-day rule affect my crypto tax report?

If you buy the same token within 30 days of a disposal, that acquisition must be matched against the disposal first, before the Section 104 pool is used. This changes the cost base for that disposal and can significantly affect the gain or loss reported. Your crypto tax report should show each matched pair separately from pool-based calculations.

Can I offset crypto losses against gains using the Section 104 pool?

Yes. If a pool-based disposal produces an allowable loss, that loss can be offset against capital gains in the same tax year, including gains from other asset classes. Any unused losses can be carried forward to future tax years, but they must be reported to HMRC within four years of the tax year in which they arose.

What records do I need to keep to support my Section 104 pool calculation?

HMRC expects you to retain records of every transaction including the date, the type and quantity of tokens involved, the value in sterling at the time, the fees paid, and the exchange or wallet used. These records should be kept for at least five years after the filing deadline for the relevant tax year in case HMRC opens an enquiry.

How do I know if my crypto tax software applies Section 104 rules correctly?

Look for software that explicitly applies the same-day rule first, then the 30-day rule, and only then allocates remaining disposals to the Section 104 pool. The software should also allow you to review each disposal individually and should generate a crypto tax report that shows the matching rule applied to each transaction.

Is staking income included in the Section 104 pool?

Staking rewards are typically treated as miscellaneous income at the point of receipt, with the market value on that date forming the cost base for those tokens. When you later sell the staked tokens, they enter the Section 104 pool at that cost base and are treated like any other acquisition from that point forward.

Source: CryptaTax