Crypto Airdrop Tax in Australia: What You Actually Owe

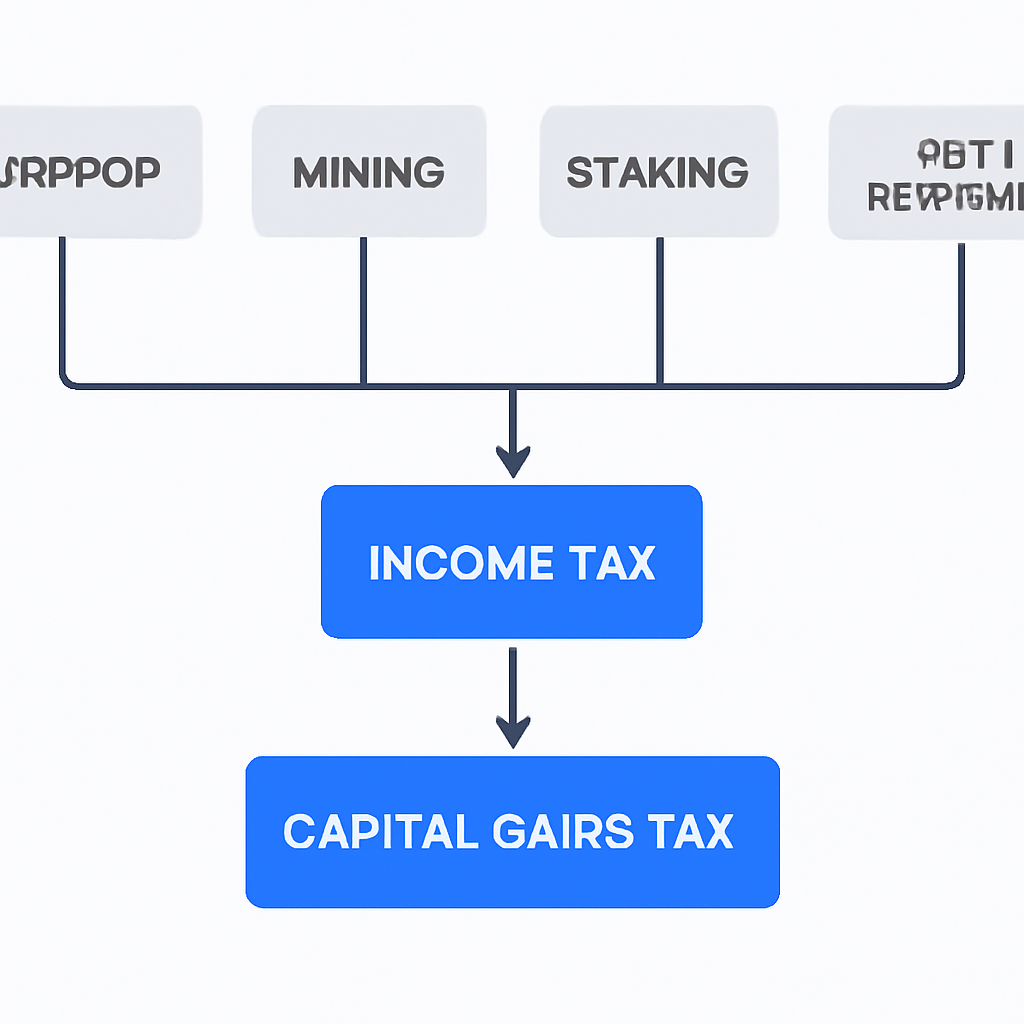

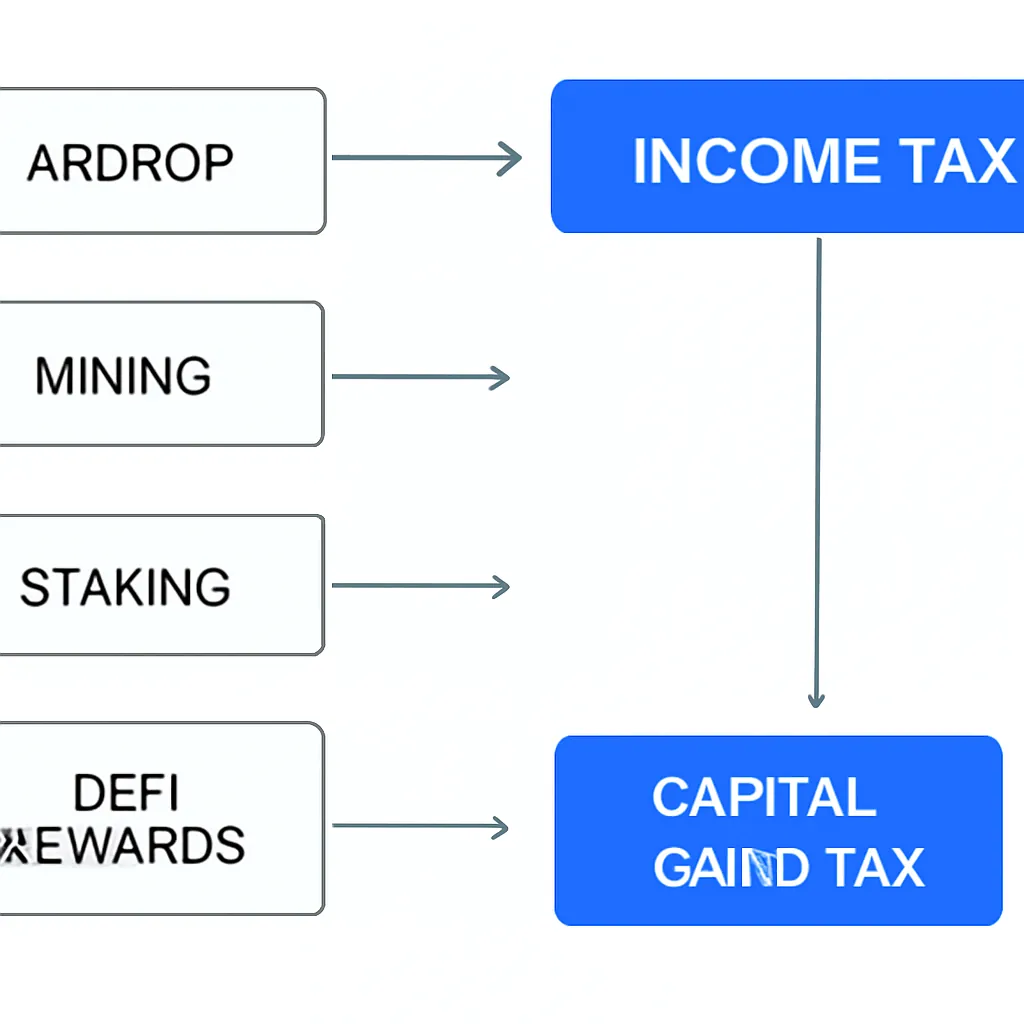

Crypto airdrop tax catches a surprising number of Australian holders off guard. The Australian Taxation Office treats most airdropped tokens as ordinary income, meaning the market value of what you receive is taxable the moment it lands in your wallet, not when you eventually sell. The same logic extends to mining rewards, staking income, DeFi earnings, and even some NFT activity. Whether you are a casual trader who received a handful of tokens through a promotional drop or a serious miner running rigs around the clock, the ATO expects you to report correctly. Australia's tax rules on crypto are detailed and, for those who ignore them, increasingly enforced. This guide walks through each income type, explains how the ATO categorises it, and tells you what records you need to avoid a headache at tax time.

How the ATO Classifies Crypto Assets

The ATO does not treat cryptocurrency as currency. It treats it as property, specifically as a capital gains tax asset in most situations. That classification matters because it determines which tax rules apply at which point. When you acquire a crypto asset, the ATO wants to know the date of acquisition and the market value in Australian dollars at that moment. When you dispose of it, whether by selling, trading, gifting, or spending, you calculate either a capital gain or a capital loss.

Income-Generating Crypto Activity

Where things get more complex is with income-generating crypto activity. Airdrops, mining, staking, and DeFi rewards often create a taxable income event before any disposal happens. The ATO views the receipt of these tokens as similar to receiving wages or business income. You include the fair market value in your assessable income for the financial year in which you received the tokens. A second tax event then occurs later when you sell or trade those same tokens, at which point capital gains tax rules apply to any increase in value since acquisition.

The table below summarises how the ATO categorises the most common crypto income types.

| Income Type | ATO Treatment on Receipt | CGT Event on Disposal |

|---|---|---|

| Airdrop (promotional) | Ordinary income at market value | Yes, cost base is market value at receipt |

| Airdrop (unsolicited, no service) | Generally no income tax; CGT applies on disposal | Yes, cost base may be zero |

| Mining rewards | Ordinary income (business) or hobby income | Yes |

| Staking rewards | Ordinary income at market value | Yes |

| DeFi lending rewards | Ordinary income at market value | Yes |

| NFT sale proceeds | Income or CGT depending on activity | Yes, if held as investment |

Crypto Airdrop Tax: When Does It Apply?

The ATO distinguishes between two broad types of airdrops. If you received tokens in exchange for something, such as signing up to a platform, completing a task, holding a qualifying token, or participating in a protocol, the receipt is treated as ordinary income. You report the Australian dollar value of the tokens on the date they entered your wallet. That value also becomes your cost base for any future CGT calculation.

Unsolicited Airdrops Treatment

Unsolicited airdrops are treated differently. If tokens simply arrived in your wallet without any action on your part and you had no prior connection to the project, the ATO has historically taken the view that no income tax arises on receipt. Instead, a CGT event occurs only when you later dispose of the tokens. In that case, your cost base could be zero or close to it, meaning any gain on disposal is fully taxable.

The practical difficulty is that the line between solicited and unsolicited is not always obvious. Participating in a governance vote, holding a token on a snapshot date, or even being an early user of a protocol can all be interpreted as actions that connect you to a project. If there is any doubt, treating the receipt as income is the more conservative and defensible position. Keeping detailed records of when and how tokens arrived, along with their market value in AUD at that time, is not optional. It is the only way to prove your position if the ATO asks questions.

Mining Income: Business or Hobby?

Mining income tax treatment in Australia depends heavily on whether your mining activity constitutes a business. The ATO looks at several factors: the scale of your operation, whether you run it in a businesslike way, your intention to make a profit, and how much time and capital you invest. A person running a single GPU as a side activity is unlikely to be classified as carrying on a business. Someone operating multiple rigs, claiming expenses, and treating mining as a primary income source almost certainly is.

Business Miners Tax Treatment

For business miners, rewards received are treated as ordinary income at the market value on the date of receipt. Business expenses, including electricity, hardware, and related costs, are generally deductible. When the mined coins are eventually sold, a CGT event arises. The cost base is the income value already declared, so you are not taxed twice on the same amount. You pay CGT only on the appreciation above that initial income figure.

Hobby miners do not get to deduct expenses, but they also do not declare mining receipts as ordinary income. Instead, they pay CGT when they eventually sell. The cost base is generally treated as the market value at the time of receipt. The distinction matters significantly at scale, because a misclassification can result in either underpayment or overpayment, both of which create problems with the ATO.

Crypto Staking Tax and Is Staking Taxable in Australia

Staking rewards are one of the most commonly misunderstood areas of crypto tax in Australia. The question of whether staking is taxable has a clear answer from the ATO: yes, in most cases. When you receive staking rewards, the ATO treats those tokens as ordinary income at their market value in Australian dollars on the day you receive them. This applies regardless of whether you are staking directly through a validator, using a liquid staking protocol, or delegating through a centralised exchange.

Tracking Staking Rewards

The practical challenge with staking is frequency. Many staking protocols distribute rewards daily or even multiple times per day. Each distribution is technically a separate income event. Tracking the AUD value of every reward at the precise moment of receipt is genuinely difficult without software. Keeping a real-time record is not just good practice, it is what the ATO expects if your return is ever reviewed.

When you later sell or swap your staking rewards, a second tax event arises. The cost base for those tokens is the income value you already declared. Any increase in price between receipt and disposal is subject to CGT. If you held the tokens for more than twelve months before disposing of them, you may be eligible for the 50% CGT discount, which is one of the more significant tax planning opportunities available to Australian crypto holders.

How Are DeFi Rewards Taxed?

DeFi tax is one of the fastest-evolving areas of crypto taxation in Australia, partly because the protocols themselves are complex and the ATO's guidance has not always kept pace. The general principle, however, is consistent with other income-generating crypto activity: if you receive tokens as a return for providing liquidity, lending assets, or participating in a yield protocol, those tokens are treated as ordinary income at the point of receipt.

DeFi Rewards Nuances

How DeFi rewards are taxed becomes more nuanced when you consider what happens inside a protocol. Providing liquidity to an automated market maker typically involves depositing two tokens and receiving liquidity provider tokens in return. The ATO may treat this as a disposal of the original tokens, triggering a CGT event at the point of deposit. When you withdraw liquidity and receive your original tokens back, that too may be a disposal. Any rewards earned in the meantime are assessed as income.

Wrapped tokens add another layer. Wrapping a token to use it in a DeFi protocol may constitute a disposal if the wrapped version is considered a different asset. The ATO has not issued definitive guidance on every scenario, which means many DeFi participants are operating with genuine uncertainty. CryptaTax is built to handle this complexity, importing transaction data from wallets and protocols and applying the relevant ATO rules automatically, so you spend less time on spreadsheets and more time on the activity itself.

NFT Tax in Australia

NFT tax depends on what you are doing with NFTs and why. If you buy an NFT as an investment and later sell it at a profit, the gain is subject to CGT. If you hold it for more than twelve months, the 50% discount may apply. If you are creating and selling NFTs as part of a business, the proceeds are ordinary income and the costs of creation are deductible. The ATO treats NFT activity through the same lens it uses for other assets: what was your intention, and does the activity look like a business?

Play-to-Earn Game Complexity

Play-to-earn games introduce further complexity. Tokens earned through gameplay may be treated as income at receipt, similar to staking rewards. NFTs received as prizes or rewards may also carry an income tax liability before any sale occurs. The key question is always the market value in AUD at the time of receipt. Without that figure, you cannot calculate your liability accurately.

| NFT Activity | Likely Tax Treatment | Key Consideration |

|---|---|---|

| Buying and selling as investment | CGT on disposal | 12-month discount may apply |

| Creating and selling NFTs | Ordinary income | Creation costs may be deductible |

| Receiving NFT as prize or reward | Ordinary income at market value | Cost base set at income value |

| Play-to-earn token rewards | Ordinary income at receipt | Frequent events require tracking |

Crypto Trading Tax and Record-Keeping Obligations

Crypto trading tax in Australia applies every time you dispose of a crypto asset. A disposal includes selling for fiat, trading one crypto for another, spending crypto on goods or services, and gifting crypto to someone other than a spouse. Each of these is a separate CGT event, and you need to record the AUD value at the time it happened. The ATO does not accept approximations or estimates. It expects accurate, contemporaneous records.

Required Records for Trading

The records you need to keep include: the date of each transaction, the amount in AUD at the time, what the crypto was used for, and the identity of the other party where possible. Exchange records, wallet addresses, and transaction hashes all support your position. The ATO has access to data from Australian exchanges and uses data-matching technology to cross-reference declared income against exchange records. Failing to report accurately is therefore increasingly risky.

For active traders with hundreds or thousands of transactions across multiple wallets and exchanges, manual tracking is not realistic. Automated tools that pull transaction history, calculate cost bases using either FIFO or specific identification methods, and produce an ATO-ready report are the practical solution. Sorting this out before 30 June, rather than scrambling in July, also gives you time to make any strategic decisions, such as realising losses to offset gains.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Priya is a software developer based in Sydney who has been active in crypto since 2021. During the financial year, she received a token airdrop from a DeFi protocol she had used previously, earned staking rewards weekly from her ETH holdings, and sold two NFTs she had purchased six months earlier. She also swapped several tokens on a decentralised exchange, which she had not realised were taxable events.

When Priya sat down to prepare her return, she had transaction records spread across three wallets and two centralised exchanges. She had no record of the AUD value of her staking rewards at the time of each distribution, and she was unsure whether her airdrop counted as income. Using CryptaTax, she imported all her wallet and exchange data in one place. The platform identified each income event, pulled historical AUD prices, and categorised each transaction according to ATO rules. Her airdrop was flagged as likely income given her prior use of the protocol. Her staking rewards were calculated across every distribution. Her NFT disposals were assessed for the CGT discount eligibility. Within an afternoon, Priya had a complete tax report she could hand to her accountant, confident that nothing had been missed.

Frequently Asked Questions

Is a crypto airdrop taxable in Australia?

In most cases, yes. If you received an airdrop in connection with using a platform, holding a qualifying token, or completing any action, the ATO treats the tokens as ordinary income at their market value on the date of receipt. Genuinely unsolicited airdrops where you took no action may only trigger CGT on disposal, but the distinction requires careful consideration and good records.

When does the 50% CGT discount apply to crypto?

The 50% CGT discount is available to individual Australian taxpayers who hold a crypto asset for more than twelve months before disposing of it. This can significantly reduce the tax payable on a gain. It applies to the disposal event, not to the income tax liability on staking or airdrop receipts, which are assessed separately at the time of receipt.

Is staking taxable in Australia?

Yes. The ATO treats staking rewards as ordinary income at the market value in Australian dollars on the date each reward is received. A second tax event arises when you later sell or swap those staking tokens, at which point CGT rules apply to any gain above the cost base established at receipt. The 50% discount may apply if you held the rewards for over twelve months before disposal.

How are DeFi rewards taxed in Australia?

DeFi rewards received for providing liquidity, lending, or yield farming are generally treated as ordinary income at the time of receipt. The AUD market value at that moment is both the income figure and the cost base for future CGT purposes. Some DeFi actions, such as depositing into a liquidity pool, may also trigger a CGT event on the tokens deposited, depending on how the ATO views the exchange of assets involved.

Do I pay tax on NFTs in Australia?

Yes. NFT tax in Australia depends on context. Buying and selling NFTs as investments attracts CGT on disposal, with the potential 50% discount for assets held over twelve months. Creating and selling NFTs as a business generates ordinary income. NFTs received as prizes, rewards, or from play-to-earn games may also be treated as income at the time of receipt based on their market value.

What records does the ATO require for crypto?

The ATO expects you to keep records of every transaction, including the date, the AUD value at the time, the nature of the transaction, and the parties involved where identifiable. Exchange statements, wallet transaction histories, and blockchain records all count. Records should be kept for at least five years after the relevant tax return is lodged. Incomplete records can lead to ATO assessments based on their own calculations, which may not be in your favour.

Does swapping one crypto for another trigger a tax event?

Yes. The ATO treats a crypto-to-crypto trade as a disposal of the first asset and an acquisition of the second. A CGT event arises on the token you give away, calculated as the AUD market value at the time of the swap minus your cost base. This applies to trades on both centralised and decentralised exchanges, including token swaps inside DeFi protocols.

Are mining rewards taxed as income or capital gains in Australia?

This depends on whether your mining constitutes a business. Business miners declare rewards as ordinary income at market value on receipt and can claim relevant expenses. Hobby miners generally do not declare income on receipt but pay CGT when they eventually sell, with the cost base set at the market value when the coins were received. The classification depends on the scale, regularity, and commercial nature of your activity.

Source: CryptaTax