DeFi Tax in Ireland: What You Owe and How to Get It Right

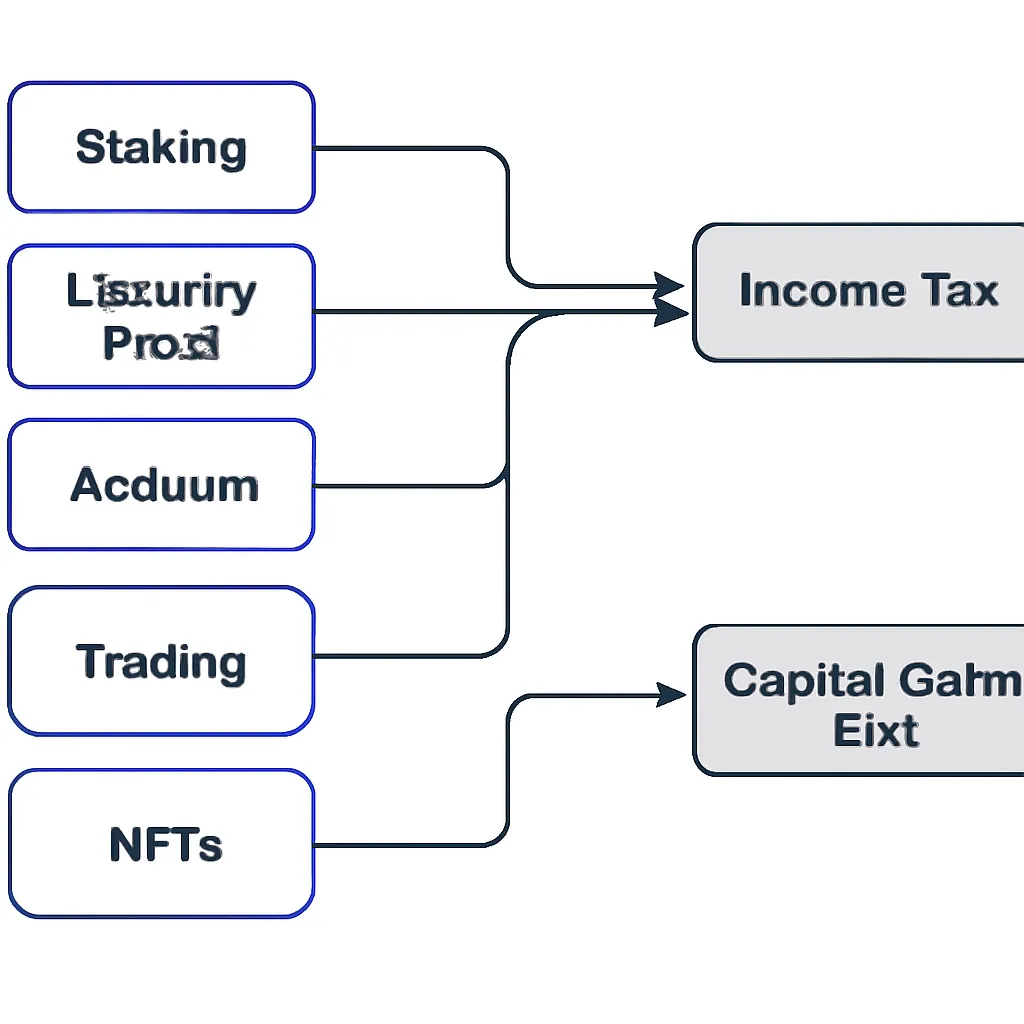

DeFi tax in Ireland is not a single rule. It is a collection of overlapping treatments that depend on what you actually did with your crypto. Did you stake tokens and earn rewards? Provide liquidity? Swap one asset for another on a decentralised exchange? Each of those activities can attract a different tax, at a different rate, on a different schedule. Irish Revenue has not published a dedicated DeFi guidance document, but the existing framework covering income tax, capital gains tax, and corporation tax applies fully to these activities. Ignoring them because the rules feel uncertain is not a safe position. Revenue has made clear that crypto assets are taxable, and the onus is on the individual to self-assess correctly. This guide explains how the main DeFi activities are treated, what records you need, and what the deadlines look like for Irish filers.

How Irish Revenue Classifies Crypto and DeFi Activity

Revenue treats crypto assets as property for tax purposes, not as currency. That single classification drives almost everything. When you dispose of a crypto asset, whether by selling it, swapping it for another token, or spending it, you trigger a Capital Gains Tax event. The gain is the difference between your disposal proceeds and your allowable cost, adjusted for any incidental expenses. The CGT rate in Ireland is 33%, and every individual has an annual exemption of €1,270 that can be applied before tax is calculated.

Income Tax on Crypto Rewards

The income side is separate. When you receive crypto as a reward for an activity, Revenue generally treats that receipt as income in the first instance. The token's market value at the moment you receive it becomes both your taxable income and your acquisition cost for future CGT purposes. This two-step treatment is central to understanding defi tax: you may pay income tax when you receive a reward, and then CGT again when you later sell or swap the same token.

The table below summarises the two main tax types that apply to DeFi activities in Ireland.

Tax Type Comparison Table

| Tax Type | Trigger | Rate | Annual Exemption |

|---|---|---|---|

| Capital Gains Tax (CGT) | Disposal of a crypto asset (sale, swap, spend) | 33% | €1,270 per individual |

| Income Tax / USC / PRSI | Receipt of crypto as income (rewards, airdrops, salary) | Up to 52% combined | None on income |

Crypto Staking Tax: Is Staking Taxable in Ireland?

Staking is taxable in Ireland. The question is not whether you owe tax on staking rewards, but when and at what rate. When your staking rewards land in your wallet, Revenue's position is that you have received income. The value of those tokens on the date of receipt is assessable as miscellaneous income, subject to income tax at your marginal rate, plus Universal Social Charge and PRSI where applicable. For a higher-rate taxpayer, the combined effective rate on that income can reach around 52%.

Cost Basis from Staking Rewards

The cost basis you establish at that point matters a great deal. If you received staking rewards worth €500 and paid income tax on €500, your CGT base cost for those tokens is €500. If you later sell them for €800, you owe CGT only on the €300 gain, not on the full €800. Keeping precise records of the token price at the time each reward was received is therefore not optional. It directly affects your CGT calculation.

Liquid Staking Tax Considerations

Liquid staking protocols, where you receive a derivative token representing your staked position, add another layer. Receiving the derivative token may itself constitute a taxable event if it is treated as a disposal of the original asset. The rules here are not settled with explicit Revenue guidance, but applying the general disposal principle is the cautious approach.

How Are DeFi Rewards Taxed: Liquidity Pools and Yield Farming

Understanding how are defi rewards taxed requires looking at each step of a liquidity pool transaction separately. When you deposit tokens into a liquidity pool, you typically receive liquidity provider (LP) tokens in return. Revenue would likely treat that deposit as a disposal of the original tokens and an acquisition of the LP tokens. That means a CGT event at the point of deposit, based on the market value of the tokens you put in.

Tax Events During Pool Deposit and Withdrawal

Fees and yield accumulated while your assets sit in the pool are treated as income, taxable at your marginal rate in the period they accrue or are received. When you withdraw from the pool, you dispose of your LP tokens and reacquire the underlying assets, which is another CGT event. If the pool is exposed to impermanent loss, that loss may reduce your gain on disposal, but you cannot claim a loss against income.

Yield farming compounds this further. Harvesting reward tokens from a farm is an income receipt. Reinvesting them into another protocol is a disposal of those reward tokens. Every harvest and every reinvestment is a separate taxable event that needs a date, a token price, and a value recorded.

DeFi Activity Tax Summary Table

| DeFi Activity | Tax on Entry / Receipt | Tax on Exit / Disposal |

|---|---|---|

| Staking rewards | Income tax at marginal rate on receipt value | CGT on gain above cost basis |

| Liquidity pool deposit | CGT event on disposal of deposited tokens | CGT event on disposal of LP tokens at withdrawal |

| Yield farming harvest | Income tax on value of reward tokens received | CGT on gain if reward tokens are later sold |

| Airdrop | Income tax on market value at receipt date | CGT on gain above that receipt value at sale |

| NFT sale | Not applicable on purchase | CGT at 33% on gain, or income tax if trading activity |

Crypto Airdrop Tax in Ireland

Crypto airdrop tax follows the same income-first logic. If you receive tokens for free, whether as a promotional airdrop, a governance token distribution, or a protocol reward, Revenue treats the fair market value of those tokens on receipt as miscellaneous income. You owe income tax, USC, and PRSI on that amount in the tax year you receive them.

Taxable Receipt Regardless of Action

Some airdrops arrive without any action on your part. Others require you to complete a task, such as holding a specific token or interacting with a protocol. Revenue does not appear to distinguish between the two for income tax purposes. The receipt of valuable tokens is the taxable event regardless of whether you actively claimed them.

Valuing Illiquid Airdropped Tokens

One practical difficulty is that many airdropped tokens have volatile or illiquid prices on the day of receipt. You are still required to use the best available market price at that date. If no reliable price exists, documenting your methodology is important in case Revenue ever questions your return. Using a recognised aggregator price or an exchange spot price at the time of receipt is a defensible approach.

NFT Tax and Crypto Trading Tax in Ireland

NFT tax in Ireland sits within the general CGT framework. Buying and selling an NFT is treated as the acquisition and disposal of a chargeable asset. If you sell an NFT for more than you paid, the gain is subject to CGT at 33% after your €1,270 exemption. If you created and sold NFTs regularly as a business activity, Revenue could reclassify that income as trading income subject to income tax rather than CGT. The distinction between occasional investing and habitual trading matters.

CGT on Crypto Trading Swaps

Crypto trading tax, meaning tax on profits from buying and selling tokens on decentralised exchanges, follows the same CGT logic. Every swap between two tokens is a disposal. Swapping ETH for USDC, for example, is a disposal of ETH at the prevailing market rate. You calculate the euro value of the ETH at the time of the swap, subtract your acquisition cost, and the difference is your gain or loss. Losses can be offset against gains in the same tax year or carried forward to future years, but they cannot be used to reduce your income tax liability.

Record-Keeping and Filing Deadlines

Accurate records are the foundation of any DeFi tax return. You need, for every transaction: the date, the tokens involved, the euro value at the time of the transaction, the type of activity, and the wallet or exchange where it occurred. DeFi protocols do not send you a tax certificate. The responsibility to reconstruct your transaction history falls entirely on you.

CGT Payment and Filing Deadlines

For CGT, any gains realised between 1 January and 30 November must be paid by 15 December of the same year. Gains realised in December must be paid by 31 January of the following year. Your CGT liability is then formally reported in your annual self-assessment return, due by 31 October for paper filers or mid-November for ROS filers. Income from staking, airdrops, and DeFi rewards is reported on your Form 11 or Form 12, depending on your circumstances, within the same self-assessment cycle.

Consequences of Missing Deadlines

Missing these deadlines attracts interest charges. Revenue charges daily interest on late CGT payments, which accumulates quickly on large crypto positions. Filing on time, even if your records are imperfect, is better than not filing at all.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Ciara is a 34-year-old software engineer based in Dublin who has been active in DeFi for two years. During the most recent tax year, she staked ETH through a liquid staking protocol and received staking rewards monthly. She also deposited tokens into a liquidity pool on a decentralised exchange and harvested yield farming rewards twice during the year. At year end, she sold some of her accumulated reward tokens to cover income tax she expected to owe.

Ciara assumed her only tax event was the final sale. When she started preparing her return, she realised that each monthly staking reward was a separate income receipt, each liquidity pool deposit was a potential CGT event, and each yield harvest was also taxable income. She had dozens of taxable events across the year, not one.

Using CryptaTax, Ciara imported her wallet transactions directly, matched each reward receipt to a price at the date of receipt, and calculated her blended income and capital gains position across all protocols. The software separated her income tax exposure from her CGT liability and generated figures she could enter directly into her self-assessment return, saving her hours of manual spreadsheet work and reducing the risk of an error that could trigger a Revenue enquiry.

Frequently Asked Questions

Is DeFi taxable in Ireland?

Yes. Revenue treats all crypto activity, including DeFi, as taxable. There is no exemption for decentralised protocols. The tax type depends on the specific activity: income tax applies to rewards and airdrops on receipt, while CGT applies to disposals of crypto assets.

How is staking taxed in Ireland?

Crypto staking tax in Ireland works in two stages. When you receive staking rewards, their market value at that date is treated as miscellaneous income and taxed at your marginal rate, plus USC and PRSI. When you later sell or swap those reward tokens, any gain above your original income cost is subject to CGT at 33%.

Is staking taxable even if I don't sell the rewards?

Yes, is staking taxable even when you hold the tokens is one of the most common questions Irish crypto users ask. Revenue's position is that the income arises when you receive the tokens, not when you sell them. You owe income tax in the year of receipt regardless of whether you sell.

How are DeFi rewards taxed when they come from a liquidity pool?

Fees and yield earned inside a liquidity pool are treated as income in the period they are received. The deposit of tokens into the pool is likely a CGT disposal event, and withdrawal is another. How are defi rewards taxed also depends on whether the protocol issues LP tokens, which can add another layer of CGT calculation.

What is the NFT tax rate in Ireland?

NFT tax in Ireland is generally CGT at 33% on any gain made when you sell an NFT. Your cost is what you paid to acquire it, including any gas fees. If Revenue determines you are buying and selling NFTs as a trade rather than investing, income tax rates apply instead, which can be significantly higher.

How is a crypto airdrop taxed in Ireland?

Crypto airdrop tax is assessed as income in the year you receive the tokens. You use the fair market value of the tokens on the date of receipt as your taxable amount and report it on your self-assessment return. That same value then becomes your CGT base cost if you later sell.

What records do I need for my DeFi tax return?

You need the date of every transaction, the tokens involved, the euro value at the time, the type of activity, and the platform or wallet used. DeFi protocols do not provide tax summaries, so you must compile this yourself. Crypto tax software that connects directly to your wallets makes this significantly more manageable.

When do I pay CGT on crypto in Ireland?

For gains made between January and November, CGT must be paid by 15 December of that year. Gains made in December are due by 31 January of the following year. Both are then reported in your annual self-assessment return, due in October or mid-November depending on whether you file through ROS.

Can I offset crypto losses against DeFi gains in Ireland?

Yes. Capital losses on crypto disposals, including DeFi swaps and sales, can be offset against capital gains in the same tax year. Any unused losses carry forward to future years. Losses cannot be used to reduce income tax on staking rewards or airdrop income.

Does swapping one crypto for another trigger a tax event in Ireland?

Yes. Crypto trading tax applies to every swap, including token-to-token swaps on decentralised exchanges. Each swap is a disposal of the token you give away and an acquisition of the token you receive. You calculate the euro value of the disposed token at the time of the swap to determine your gain or loss.

Source: CryptaTax