Crypto Tax Switzerland: A Complete Guide for Individuals

For many crypto holders, Switzerland sounds like a tax haven. And in some respects, it genuinely is. Crypto tax in Switzerland is structured in a way that can mean zero capital gains tax for private investors, but that outcome is not automatic. The rules hinge on whether the tax authority, the Swiss Federal Tax Administration, classifies you as a private investor or a professional trader. Get that classification wrong and what looked like a tax-free gain becomes taxable income. This guide explains how crypto is taxed in Switzerland, what triggers professional trader status, how wealth tax applies to digital assets, and how the Swiss framework compares to crypto tax rules in India and the UK.

How Is Crypto Taxed in Switzerland for Private Investors

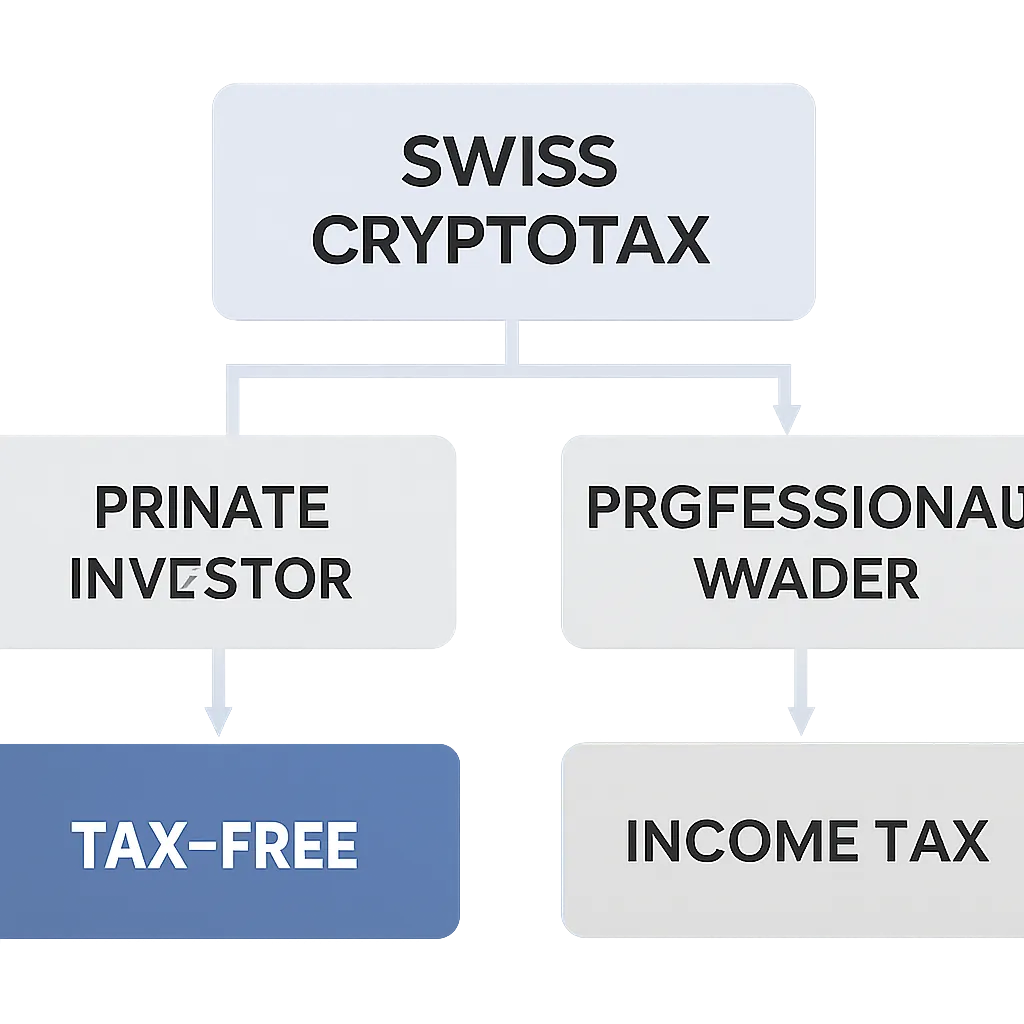

The starting point under Swiss tax law is that capital gains realised by private individuals are not subject to income tax. This principle applies to crypto assets just as it does to shares and other securities. A private investor who buys Bitcoin, holds it, and sells it at a profit owes no capital gains tax on that profit at the federal level. Cantons follow the same treatment. This is one of the most favourable positions for individual crypto holders anywhere in the developed world.

Tax-Free Capital Gains for Private Investors

There is a catch, though. Income derived from crypto is still taxable. If you receive crypto as payment for services, as mining rewards, as staking income, or as part of your employment, that income is treated as ordinary income and taxed accordingly. The tax-free status applies only to capital appreciation, not to crypto received as compensation for an activity. Airdrops and hard fork receipts sit in a grey area and are generally assessed based on whether there was an economic activity behind them.

Taxable Crypto Income Situations

Crypto-to-crypto trades are also worth understanding. Swapping one token for another is treated as a disposal and a simultaneous acquisition. Any gain realised at the point of the swap would theoretically be a capital gain, and for private investors, it would still fall under the capital gains exemption. The Swiss framework does not penalise frequent trading per se, but frequency is one of the factors the tax authority uses when deciding whether someone has crossed into professional trader territory.

Crypto Tax Switzerland: When Professional Trader Status Applies

The Swiss Federal Tax Administration uses a set of criteria to determine whether an investor should be reclassified as a professional trader. Once that status applies, gains are taxed as income, and the capital gains exemption disappears entirely. The criteria are not applied as a rigid checklist. Instead, the tax authority looks at the overall picture.

Criteria for Professional Trader Status

Key indicators include how frequently you trade, whether you use leverage or derivatives, how long you typically hold positions, whether trading generates a significant portion of your income, and whether the volume of transactions is consistent with investment activity or resembles a business operation. There is also a rule of thumb around holding period. Positions closed within six months of purchase attract closer scrutiny, though six months is a guideline rather than an absolute threshold.

The table below summarises the main factors the Swiss tax authority weighs when assessing trader classification.

Trader Classification Factors Table

| Factor | Private Investor Signal | Professional Trader Signal |

|---|---|---|

| Holding period | Long-term holds, typically over six months | Frequent short-term trades, under six months |

| Use of leverage | Spot purchases only | Margin trading, derivatives, futures |

| Income dependency | Crypto gains are incidental to salary | Crypto gains form a significant share of income |

| Transaction volume | Occasional, low-volume activity | High transaction count, systematic approach |

| Financing method | Own capital only | Borrowed funds used to acquire positions |

Crypto Wealth Tax and How to Report Digital Assets

Even when capital gains are exempt, crypto holders in Switzerland cannot ignore the wealth tax. Switzerland levies an annual wealth tax at the cantonal level on the total value of a taxpayer's net assets. Crypto assets count as taxable wealth and must be declared in the annual tax return, valued at their fair market value on 31 December of the tax year.

Wealth Tax on Crypto Holdings

The Swiss Federal Tax Administration publishes official year-end rates for major cryptocurrencies such as Bitcoin and Ether. For tokens without an official rate, taxpayers use the market price from a recognised exchange. Failing to declare crypto holdings understates your taxable wealth, which can lead to penalties and back taxes.

How to Report Crypto in Tax Returns

Reporting itself happens through the cantonal tax return. Crypto holdings go into the securities and assets section. You declare the total value, not individual trades. If you also received crypto income such as staking rewards during the year, that income must be declared separately under income. Good record-keeping matters here. You need to be able to show the value of each asset at year-end and support any income figures with transaction records.

How Is Crypto Taxed in India: Key Rules for Comparison

For individuals researching crypto tax across multiple jurisdictions, understanding how crypto is taxed in India helps put the Swiss framework into context. India applies a flat tax rate on gains from virtual digital assets, a category that covers cryptocurrencies and NFTs. Losses from one virtual digital asset cannot be offset against gains from another, and losses cannot be carried forward to future years. This makes India's approach structurally different from Switzerland's, where the private investor framework is relatively permissive.

India's Flat Tax on Virtual Digital Assets

India also applies a tax deducted at source on crypto transactions above a specified threshold, placing a withholding obligation on exchanges and buyers. For Indian residents holding crypto or considering their tax position, an india crypto tax calculator can help model the impact of the flat rate and the no-offset rule across a portfolio. The table below contrasts the top-level treatment in India and Switzerland.

Comparison Table: Switzerland vs India

| Feature | Switzerland | India |

|---|---|---|

| Capital gains tax for private investors | Exempt at federal and cantonal level | Flat rate applies to all gains |

| Loss offsetting | Capital losses not relevant under exemption | No offset between different virtual digital assets |

| Crypto income (staking, mining) | Taxed as ordinary income | Taxed under the virtual digital asset rules |

| Withholding tax | Not applicable | Tax deducted at source on qualifying transactions |

| Wealth tax on holdings | Yes, annual cantonal wealth tax | No equivalent annual wealth tax on crypto |

Crypto Tax UK: How the British Framework Differs

Crypto tax in the UK is administered by HMRC, and the approach differs from both Switzerland and India. HMRC treats crypto assets as a form of property. Disposals, which include sales, crypto-to-crypto swaps, spending crypto, and gifting crypto to anyone other than a spouse, trigger a capital gains tax calculation. Gains above the annual exempt amount are taxed at rates that depend on whether they fall within the basic rate or higher rate income tax band.

UK Capital Gains Tax on Crypto Disposals

UK taxpayers who mine crypto, receive staking rewards, or are paid in crypto must report that as income, subject to income tax and National Insurance in some cases. HMRC has also confirmed that crypto received through airdrops can be taxable income where there is an expectation of a service in return. A uk crypto tax calculator helps individuals model their total liability across both income and capital gains categories, particularly when they have activity spread across multiple exchanges and wallets. The UK also uses a specific share identification method called the share pooling or section 104 pool rule, which averages the cost basis across all units of the same token held.

Record-Keeping: What Swiss Crypto Holders Need to Track

Regardless of whether you expect to owe tax, solid record-keeping is essential for Swiss crypto holders. The wealth tax declaration alone requires accurate year-end valuations for every asset. If you ever face a review and need to demonstrate private investor status, transaction records showing purchase dates, holding periods, and the absence of leverage will be your primary evidence.

Essential Records for Wealth Tax Declaration

You should keep records of every acquisition with date and price, every disposal with date and price received, any crypto income received including staking, lending, and referral rewards, and the value of all holdings on 31 December each year. Records should be kept for at least ten years, which is the standard statute of limitations under Swiss tax law. Most Swiss crypto holders find that aggregating data from multiple exchanges and wallets manually is error-prone. Using software that connects to exchange APIs and calculates year-end valuations automatically reduces both the time burden and the risk of declaring incorrect figures.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Priya is a software engineer based in Zurich. She has held Bitcoin and Ether since 2021, buying periodically through a Swiss exchange and holding without active trading. In the 2024 tax year, she sold a portion of her Bitcoin after holding for over two years, realising a significant gain. She also earned staking rewards on her Ether throughout the year. Priya is unsure which parts of her activity are taxable.

Her capital gain on the Bitcoin sale is exempt because she qualifies as a private investor. Her holding period was well above six months, she used no leverage, and crypto income represents a small fraction of her salary. However, her staking rewards are taxable as ordinary income and must be declared. She also needs to declare the full market value of her remaining crypto holdings as of 31 December for wealth tax purposes. Priya uses CryptaTax to connect her exchange account, automatically calculate her staking income in Swiss francs at the date of each reward, and produce the figures she needs for her cantonal tax return. The process takes her under an hour rather than a weekend of manual spreadsheet work.

Frequently Asked Questions

Is crypto tax-free in Switzerland?

Capital gains on crypto are tax-free for private investors in Switzerland at both the federal and cantonal level. However, crypto received as income, such as staking rewards, mining income, or payment for services, is taxable as ordinary income. Crypto assets are also subject to the annual cantonal wealth tax based on their year-end value.

How is crypto taxed in Switzerland for professional traders?

If the Swiss Federal Tax Administration classifies you as a professional trader, your gains are treated as business income and taxed accordingly. Classification depends on factors including trading frequency, use of leverage, holding periods, and whether crypto forms a significant part of your income. There is no single threshold that automatically triggers professional status.

Do I need to declare crypto on my Swiss tax return?

Yes. Even if you owe no income tax on your gains, you must declare the market value of all crypto holdings on 31 December each year in the securities and assets section of your cantonal tax return. Failing to declare understates your taxable wealth and can lead to penalties.

How is crypto taxed in India compared to Switzerland?

India applies a flat rate on gains from virtual digital assets with no ability to offset losses between different assets. Switzerland exempts capital gains for private investors entirely. India also applies a tax deducted at source on qualifying crypto transactions, which has no equivalent in Switzerland. The two regimes are structurally very different.

Can I use a crypto tax calculator for India?

Yes. An India crypto tax calculator helps you apply the flat tax rate and the no-loss-offset rule across your full transaction history to produce an accurate liability figure. It is particularly useful when you have traded across multiple exchanges, because manually applying the rules to hundreds of transactions is error-prone and time-consuming.

How does crypto tax in the UK work?

HMRC treats crypto as property. Sales, swaps, spending, and gifting crypto are all disposals that trigger capital gains tax calculations. Gains above the annual exempt amount are taxed at rates tied to your income tax band. Crypto income from staking, mining, or employment is taxed as income and may attract National Insurance contributions.

What is a UK crypto tax calculator used for?

A UK crypto tax calculator applies HMRC's share pooling rules to your transaction history and separates capital gains from income events. It produces figures ready for the self-assessment tax return, covering both the capital gains tax summary and any crypto income that must be reported under income tax. It saves significant time when activity spans multiple platforms.

What records do Swiss crypto holders need to keep?

You need records of every acquisition and disposal including dates and prices, all crypto income received during the year, and the value of all holdings on 31 December. Records should be retained for at least ten years. Swiss tax law requires you to be able to substantiate both your wealth tax declaration and, if challenged, your private investor status.

Are staking rewards taxable in Switzerland?

Yes. Staking rewards are treated as taxable income in Switzerland, assessed at the market value of the tokens at the time they are received. They must be declared in the income section of your tax return, separate from your wealth declaration. The capital gains exemption does not apply to staking income.

Does Switzerland have a crypto-specific tax law?

Switzerland does not have a standalone crypto tax law. Digital assets are taxed under existing principles: capital gains rules for private investors, income tax rules for professional traders and crypto income, and wealth tax rules for asset declarations. The Swiss Federal Tax Administration has issued guidance clarifying how these existing rules apply to crypto assets.

Source: CryptaTax