Crypto Airdrop Tax: What Every Individual Holder Needs to Know

Receiving free tokens sounds like pure upside, but crypto airdrop tax obligations can catch individual holders off guard. In most major jurisdictions, the moment you receive an airdrop is already a taxable event, not the moment you sell. The fair market value of those tokens at the time they land in your wallet is typically treated as ordinary income, and that figure also becomes your cost basis for any future disposal. Get this wrong and you risk under-reporting income, over-paying capital gains, or both. This guide walks through how airdrop taxation works, how it connects to defi tax and crypto staking tax, and what you should be tracking regardless of where you live.

Why Airdrops Are Usually Taxable at Receipt

The instinct many holders have is to treat an airdrop like a gift: you did nothing to earn it, so surely tax does not apply yet. Tax authorities largely disagree. The dominant view across the US, UK, and most EU member states is that receiving tokens of ascertainable value constitutes a form of income. If the tokens have an active market price at the moment of receipt, that price is what you received, and income tax applies accordingly.

Tax Authorities View Airdrops as Income

The logic mirrors how employment benefits in kind are taxed. If your employer gives you something of value, it counts as income even though no cash changed hands. An airdrop is treated similarly: you have enriched yourself by an amount equal to the market value of the tokens on the day you received them. Some jurisdictions carve out exceptions for tokens with no established market price or for promotional distributions that require no action on the holder's part, but these exceptions are narrower than most people assume. The safer default position is to assume taxability unless you have specific guidance from your local tax authority confirming otherwise.

The table below summarises the general approach taken in three major jurisdictions, based on publicly available guidance.

Jurisdiction Comparison Table

| Jurisdiction | Airdrop at Receipt | Valuation Basis | Later Disposal |

|---|---|---|---|

| United States | Ordinary income (federal) | Fair market value on date of receipt | Capital gains tax applies; short or long-term depending on holding period |

| United Kingdom | Income tax if received in return for services or as part of a trade; miscellaneous income otherwise | Sterling equivalent on date of receipt | Capital gains tax on disposal; cost basis is value at receipt |

| Germany | Generally income if received in exchange for an action; potentially tax-free if purely speculative with no market price | Euro equivalent on date of receipt where applicable | Tax-free after one-year holding period in many cases |

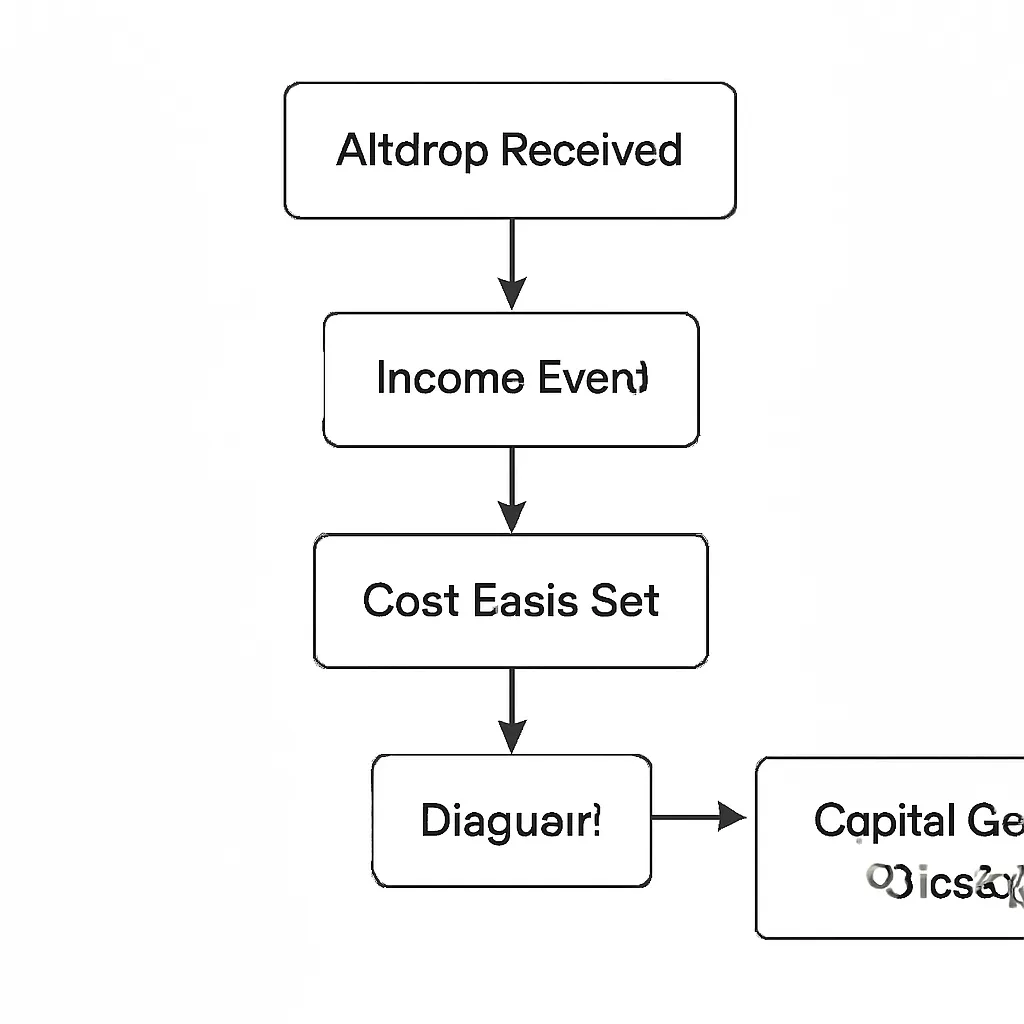

How Crypto Airdrop Tax Connects to Your Cost Basis

Understanding the cost basis mechanic is essential because it determines your crypto trading tax exposure when you eventually sell. When you receive an airdrop and report its value as income, that value becomes your cost basis in those tokens. This means you are not taxed twice on the same amount. If you receive tokens worth £500 and report £500 as income, and later sell those tokens for £700, only the £200 gain is subject to capital gains tax, not the full £700.

Cost Basis Established at Receipt

Consequences of Failing to Record Receipt

Where people run into trouble is by failing to record the receipt at all. If you have no record of having declared the income at receipt, and you later sell, there is no established cost basis. Some tax authorities will then treat the entire proceeds as a gain, which results in significant over-taxation. Others may treat the omission as under-reporting of income and apply penalties. Neither outcome is desirable. Keeping a dated record of every airdrop you receive, including the token name, quantity, and fair market value at the time, is not optional housekeeping. It is the foundation of accurate crypto trading tax reporting.

Cost basis methods vary by jurisdiction. The US generally permits specific identification or FIFO. The UK applies a pool-averaging method under its Section 104 rules. Germany uses FIFO. Knowing which method applies to you directly affects the size of your taxable gain on disposal, especially if you received multiple batches of the same token at different times.

DeFi Tax and Airdrop-Like Distributions

The line between a traditional airdrop and other token distributions in the decentralised finance space is often blurred. Many DeFi protocols distribute governance tokens to liquidity providers, yield farmers, or users who complete specific on-chain actions. The question of how are DeFi rewards taxed follows the same general framework: if you receive tokens of measurable value, that receipt is likely an income event.

DeFi Distributions Follow Airdrop Framework

Liquidity mining rewards, governance token distributions, and rebasing mechanisms all raise similar questions. A rebasing token that automatically increases your balance may or may not generate an immediate income event depending on the jurisdiction and the specific mechanics involved. Some tax authorities have issued guidance on yield farming and liquidity provision; many have not. Where guidance is absent, the conservative and defensible approach is to treat each token receipt as income at fair market value on the date received. DeFi tax is a genuinely unsettled area of law in most countries, and that uncertainty cuts in both directions: it creates risk for holders who assume nothing is taxable, and also for those who over-report in ways that inflate their cost basis incorrectly.

Crypto Staking Tax and How It Differs

Staking rewards occupy a distinct but closely related category. Is staking taxable? In the majority of jurisdictions that have issued guidance, yes. The US IRS confirmed in Revenue Ruling 2023-14 that staking rewards are included in gross income at fair market value upon receipt. The UK HMRC treats staking rewards as miscellaneous income in most circumstances. The German approach has historically been more nuanced, with some analysis treating proof-of-stake rewards differently depending on participation level.

Staking Rewards Are Taxable at Receipt

The practical difference between staking and airdrops matters at the margin. Staking rewards arrive on a predictable, often daily or weekly, schedule. That creates a high-volume record-keeping burden: each reward event is potentially a separate income entry with its own valuation. Airdrops tend to arrive infrequently as discrete events, which makes them easier to track individually but no less taxable. For holders who both stake and receive airdrops, the combined income reporting obligation can become complex quickly. Automated tracking tools that pull on-chain data and apply daily price feeds can significantly reduce the manual burden here.

Comparison Table of Distribution Types

| Distribution Type | Typical Tax Treatment at Receipt | Record-Keeping Frequency |

|---|---|---|

| Airdrop (unsolicited) | Miscellaneous income or ordinary income at fair market value | Per event (low frequency) |

| Airdrop (action-based) | Income at fair market value; may be treated as trading income if systematic | Per event |

| Staking rewards | Income at fair market value upon receipt in most jurisdictions | Per reward epoch (high frequency) |

| DeFi yield / liquidity mining | Income treatment widely adopted; some uncertainty remains | Continuous or per block |

NFT Tax Considerations in Airdrop Scenarios

NFT tax adds another layer for holders who receive non-fungible tokens via airdrop. The valuation challenge is more acute with NFTs because there may be no liquid secondary market at the moment of receipt. If a collection has just launched and floor prices are volatile or thin, pinning a fair market value to a newly received NFT is genuinely difficult. Tax authorities have not generally issued specific guidance on NFT airdrops, leaving holders to apply general principles as best they can.

Valuation Challenges for NFT Airdrops

A reasonable approach, and one increasingly accepted in practice, is to use the verifiable floor price of the collection at the time of receipt as a proxy for fair market value. If no market exists yet and the token has no ascertainable value, some practitioners argue that income should be recognised when a market price first becomes established. However, this position carries risk and should not be adopted without taking advice appropriate to your jurisdiction. When you eventually sell an NFT received via airdrop, capital gains rules apply to the difference between your proceeds and the cost basis you established at receipt, making accurate initial valuation doubly important.

What Records You Need to Keep

Good record-keeping is not a suggestion for active crypto holders; it is a legal requirement in most jurisdictions. For every airdrop you receive, you should record the date of receipt, the token name and contract address, the quantity received, and the fair market value per token in your local fiat currency on that date. You should also keep a note of the source, meaning whether the distribution came from a protocol you interacted with, a wallet snapshot, or some other mechanism, because the source can affect the tax characterisation in certain jurisdictions.

Essential Records for Each Airdrop

Records should be retained for as long as your jurisdiction's statute of limitations requires. In the UK, that is generally six years for income tax purposes. In the US, the IRS can typically go back three years for standard assessments and six years if income is substantially under-reported. Given that crypto transactions are permanently recorded on-chain, tax authorities have access to historical data that does not expire. Keeping your own records to at least the same standard is the only reliable defence if you are ever queried.

Retention Periods and Software Recommendations

Exchange statements, wallet exports, and on-chain transaction histories are all valid source documents. The key is to store them in a format you can retrieve quickly and reconcile against your tax return. Spreadsheets work for small portfolios. For holders with multiple wallets, chains, and frequent reward distributions, dedicated crypto tax software that aggregates data automatically and applies the correct cost basis method for your jurisdiction is considerably more reliable.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Priya is a software developer based in London with a diversified crypto portfolio. In March, she receives an airdrop of governance tokens from a DeFi protocol she used the previous year. At the time of receipt, the tokens are trading at £0.80 each, and she receives 2,000 of them, giving a total value of £1,600. She records this as miscellaneous income and adds it to her self-assessment return for the tax year. Her cost basis in the tokens is therefore £1,600.

Six months later, she sells all 2,000 tokens at £1.20 each, receiving £2,400. Her capital gain is £800, the difference between her proceeds and her cost basis. She reports this gain on her self-assessment and applies her annual capital gains allowance. Because she used CryptaTax to track the airdrop at receipt with the correct sterling valuation, the cost basis figure flows automatically into her disposal calculation. She does not face the common problem of having no cost basis record and being assessed on the full £2,400. The total tax she pays is materially lower than it would have been without accurate records, and she avoids any penalty for under-reporting income.

Frequently Asked Questions

Is a crypto airdrop always taxable?

In most major jurisdictions, yes, if the tokens have an ascertainable fair market value at the time of receipt. Some limited exceptions exist for tokens with no established market price or for purely promotional distributions requiring no action, but the general rule is that receipt of valuable tokens constitutes income. You should check the specific guidance issued by your local tax authority rather than assume an exception applies.

When exactly does the crypto airdrop tax liability arise?

The taxable event typically arises at the moment the tokens are credited to your wallet and you have the ability to access and dispose of them. This is known as the constructive receipt principle. If tokens are locked or subject to a vesting schedule, some jurisdictions defer the income recognition until the tokens become freely transferable, but this varies and you should not rely on it without specific guidance.

How do I value an airdrop for tax purposes?

You use the fair market value of the tokens in your local fiat currency on the date and time of receipt. For tokens listed on established exchanges, this is usually the spot price at the time of the transaction. For newly launched tokens with thin markets, the floor price or an average of available quotes may be used. NFT airdrops present the greatest valuation challenge because floor prices can be highly variable in the early days of a collection.

Do I pay tax again when I sell airdropped tokens?

Yes, but only on the gain above your cost basis. If you correctly reported the airdrop as income at receipt, that value becomes your cost basis. When you sell, capital gains tax applies to any increase above that figure. If the tokens have fallen in value since receipt, you may have a capital loss, which can often be offset against other gains depending on your jurisdiction's rules.

How are DeFi rewards taxed compared to airdrops?

DeFi rewards such as liquidity mining payouts and governance token distributions are generally treated as income at fair market value upon receipt, the same framework applied to airdrops. The distinction that matters more in practice is frequency: DeFi rewards often accumulate continuously, creating a higher volume of individual income events to record. The underlying tax logic is the same, but the record-keeping burden is significantly greater.

Is staking taxable in the same way as receiving an airdrop?

In most jurisdictions that have issued guidance, staking rewards are treated as income at fair market value upon receipt, which parallels the treatment of airdrops. The US IRS confirmed this position in Revenue Ruling 2023-14. The UK HMRC similarly treats staking rewards as miscellaneous income in most cases. Germany has historically applied a more nuanced analysis depending on the level and nature of participation.

What records do I need to keep for airdrop tax purposes?

You need the date of receipt, the token name and contract address, the quantity received, and the fair market value per token in your local currency on that date. You should also note the source of the distribution. These records should be retained for the full length of your jurisdiction's tax statute of limitations, which is typically between three and six years but can be longer in cases involving significant under-reporting.

What happens if I forgot to report an airdrop in a previous tax year?

You should consider making a voluntary disclosure or an amended return as soon as possible. Most tax authorities treat voluntary corrections more favourably than discoveries made during an audit or investigation. The longer the omission goes uncorrected, the greater the potential penalties and interest. Given that on-chain transaction data is publicly accessible, tax authorities have the technical capacity to identify unreported airdrop income, so prompt correction is generally the lower-risk path.

Does the NFT tax treatment differ for NFTs received via airdrop compared to ones I bought?

The capital gains rules on disposal are the same regardless of how you acquired the NFT. The key difference with an airdropped NFT is that your cost basis is the fair market value at the time of receipt rather than a purchase price you paid. If you correctly reported the receipt as income, that figure carries forward as your cost basis for capital gains purposes. If you did not report it, you risk having either no established cost basis or a disputed one.

Can crypto tax software handle airdrop tracking automatically?

Yes. Software that integrates with on-chain data sources can identify airdrop transactions, apply historical price feeds to establish fair market value at receipt, and carry the resulting cost basis forward into disposal calculations. This removes the manual burden of tracking individual events across multiple wallets and chains. For holders with frequent DeFi interactions or staking rewards as well as occasional airdrops, automated tracking is considerably more reliable than spreadsheet-based approaches.

Source: CryptaTax