NFT Tax Treatment in Ireland: Your Crypto Tax Guide

Crypto tax in Ireland has grown more complex as NFTs moved from niche collectibles to mainstream digital assets. Revenue, Ireland's tax authority, has not issued a standalone NFT-specific guide, but the existing tax framework applies clearly once you understand the underlying principles. Whether you bought an NFT as an investment, created and sold digital art, or flipped tokens on a secondary marketplace, your activities almost certainly trigger a tax obligation. Getting this wrong carries real risk: penalties, interest on underpaid tax, and potential compliance inquiries. This guide walks through how NFTs are classified, when capital gains tax applies, when income tax enters the picture, and what records you need to keep to file accurately.

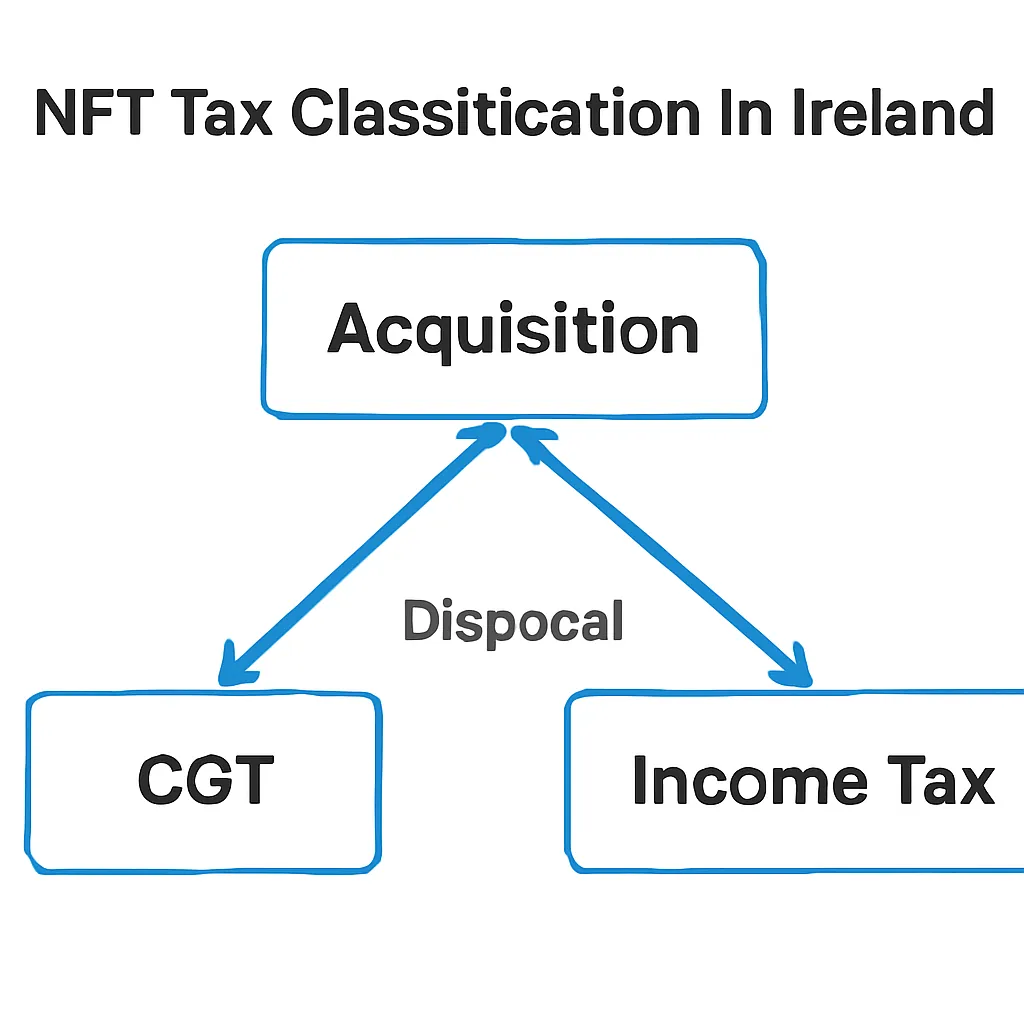

How Revenue Classifies NFTs in Ireland

Revenue does not treat NFTs as a separate asset category. Instead, it looks at the economic substance of what you hold. In most cases, an NFT is treated as a cryptoasset, meaning the same rules that govern how is crypto taxed in Ireland apply directly. The token itself, whether it represents digital art, a gaming item, or a membership pass, is property in the eyes of Irish tax law. That classification matters enormously because it determines which tax head applies to any gain or income you realise.

Capital vs Income Distinction

The key distinction Revenue draws is between capital transactions and income transactions. If you buy an NFT and later sell it at a profit, that is typically a capital event. If you create NFTs and sell them as part of a trade, or if you receive NFTs as compensation for services, those receipts are likely to be taxable as income. The same NFT activity can fall under different tax heads depending on your individual circumstances, frequency of transactions, and the intent behind your activity.

This dual-head approach mirrors how Revenue treats other cryptoassets such as bitcoin or ether. The principles are consistent, even if the underlying technology differs. One area of genuine complexity is where an NFT generates ongoing royalties for the creator: those streams are income, not capital, regardless of how the token is structured on-chain.

Capital Gains Tax on NFT Disposals in Ireland

Capital gains tax is the primary tax most Irish NFT holders will encounter. A disposal occurs whenever you sell an NFT, exchange it for another token, gift it, or otherwise transfer ownership. The current CGT rate in Ireland applies to the gain, which is the disposal proceeds minus the allowable acquisition cost and any qualifying expenses.

CGT Mechanics and Exemptions

The annual CGT exemption available to individuals in Ireland means the first portion of your net gains each tax year is free from CGT. Gains above that threshold are taxed at the applicable rate. Losses on NFT disposals can be offset against gains from other cryptoasset disposals in the same tax year, or carried forward to future years. They cannot, however, be set against income.

The table below summarises the key CGT mechanics for NFT holders in Ireland.

Common Disposal Scenarios

| Event | CGT Trigger? | Notes |

|---|---|---|

| Selling an NFT for fiat (EUR/USD) | Yes | Gain calculated on proceeds minus cost basis |

| Swapping one NFT for another NFT | Yes | Treated as disposal at fair market value |

| Selling an NFT for cryptocurrency (e.g. ETH) | Yes | Both assets may have their own gain or loss |

| Gifting an NFT | Yes | Disposal at market value; gift may also trigger CAT for recipient |

| Holding an NFT with no disposal | No | No CGT arises until a disposal event occurs |

Income Tax When You Create or Trade NFTs

For NFT creators, the tax picture is different. If you mint and sell NFTs as a regular activity, Revenue is likely to view this as trading. Trading income is subject to income tax, PRSI, and the Universal Social Charge, rather than CGT. The distinction between trading and investing is not always obvious, but Revenue typically considers factors such as frequency of activity, the nature of your work, and whether you hold assets for the short or long term with a view to quick profit.

Trading vs Investing

A digital artist who occasionally sells tokenised artwork is less likely to be treated as a trader than someone minting hundreds of NFTs per month and flipping them rapidly. However, the boundary is genuinely blurry and worth professional advice in ambiguous cases. What is clear is that you cannot simply elect which tax treatment applies: Revenue will look at the facts.

Royalties are another income category. Many NFT smart contracts encode a royalty percentage paid to the original creator each time the token resells on a secondary market. Those royalty receipts are income, taxable in the year you receive them. They are not capital. Keeping a real-time record of royalty payments across different marketplaces is therefore essential, because they are easy to overlook and easy to underreport accidentally.

How Crypto Tax Rules in Ireland Compare to Other Jurisdictions

Irish investors who also hold assets on international platforms sometimes ask how Ireland compares to other regimes they read about. The question of how is crypto taxed in India, for example, comes up frequently in communities with Irish-resident members of Indian origin. India applies a flat tax rate to gains on virtual digital assets, with no allowance to offset losses from one asset against another. That is a meaningfully different structure from Ireland's CGT framework, which does permit loss offsetting within the cryptoasset class.

Comparison With India and UK

The question of crypto tax in the UK is also relevant for Irish residents with cross-border connections or for those who lived in the UK before relocating to Ireland. HMRC and Revenue share broadly similar principles: both treat cryptoassets as property and apply capital gains rules on disposal. However, the annual exempt amounts, rates, and specific guidance differ, and tax residency determines which authority has the primary claim on your gains. If you have recently moved between Ireland and the UK, specialist advice on your residency position is worth pursuing before you file.

| Jurisdiction | Primary Tax on NFT Gains | Loss Offsetting | Creator Income Treatment |

|---|---|---|---|

| Ireland | CGT (capital gains tax) | Permitted within cryptoasset class | Income tax if trading |

| UK | CGT | Permitted against capital gains | Income tax if trading |

| India | Flat tax on virtual digital asset gains | Not permitted between different VDAs | Taxable as income |

Filing Deadlines and How to Report NFT Gains to Revenue

CGT in Ireland operates on a pay-and-file basis with two payment dates during the tax year. Gains realised in the first part of the year carry an earlier payment deadline, while gains realised in the remainder of the year have a later payment deadline. The annual tax return deadline follows after the year end. Missing the payment date, even if you file correctly, results in interest charges, so the payment obligation is separate and earlier than most filers expect.

Self-Assessment Reporting

NFT activity is reported through the standard self-assessment return. There is no dedicated NFT disclosure box. You report your net gains within the capital gains section, listing proceeds, cost, and any allowable expenses. If your NFT income is treated as trading income, it appears in the income section instead. Keeping a complete transaction log, including wallet addresses, marketplace records, and any ETH or other cryptocurrency used to purchase NFTs, is essential because the cost basis of your NFT purchase may itself involve a crypto-to-crypto disposal that needs separate reporting.

Record-Keeping for NFT Tax Purposes

Good record-keeping is the difference between a straightforward filing and a stressful one. For each NFT transaction, you need the date of acquisition, the amount paid (including gas fees), the fair market value at the time of acquisition if you paid in cryptocurrency, the date of disposal, and the proceeds received. This sounds manageable when you hold a handful of tokens, but becomes challenging quickly if you are active across multiple blockchains and marketplaces.

Tracking Costs and Gas Fees

Gas fees paid on the Ethereum network to mint, purchase, or sell an NFT are generally an allowable cost. They form part of your acquisition or disposal costs. Tracking them requires either manual reconciliation of your wallet history or a tool that automatically pulls transaction data from the blockchain. An ireland crypto tax calculator that handles NFT-specific transaction types, including swap events, royalty receipts, and gas fee allocation, will save significant time and reduce the risk of errors. CryptaTax is designed to handle exactly this kind of multi-asset, multi-chain activity for individual filers.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Aoife is a graphic designer based in Dublin who started collecting NFTs representing digital photography in 2022. She purchased three NFTs using ETH over the course of a year, paying gas fees on each transaction. In the following year, she sold two of them on a secondary marketplace, receiving ETH in return. She also received a small royalty payment when one of her own earlier digital artworks, which she had tokenised, resold on-chain.

Aoife has at least three separate tax events: the disposal of the two NFTs she purchased (CGT), the original ETH she spent to buy them (which may itself have been a disposal of ETH at a gain), and the royalty payment (income). When she sits down to file her return, she realises her wallet history spans two chains and four platforms. She uses CryptaTax to connect her wallets, automatically categorise each transaction, and calculate her net CGT position and her royalty income separately. The tool flags the ETH disposals she had not considered and generates a summary she can use to complete her Revenue return. She pays her CGT on time and avoids interest charges.

Frequently Asked Questions

Is crypto tax in Ireland the same as NFT tax in Ireland?

The same underlying principles apply. Revenue treats NFTs as cryptoassets, so the capital gains and income tax rules that govern crypto tax in Ireland apply directly to NFTs. The specific tax head depends on whether your activity is capital in nature or whether you are trading or receiving income from NFTs.

Do I pay CGT every time I swap one NFT for another?

Yes. Swapping one NFT for another is a disposal of the first NFT at its fair market value at the time of the exchange. You calculate the gain or loss on that disposal and report it. The NFT you receive in return becomes a new acquisition at its fair market value on the date of the swap.

Can I use an ireland crypto tax calculator for NFT transactions?

Yes, and it is strongly advisable if you have more than a handful of NFT transactions. An ireland crypto tax calculator that supports NFT activity will handle the cost basis allocation, gas fee treatment, and royalty income categorisation that manual spreadsheets often miss. CryptaTax is built to handle these multi-transaction scenarios for individual filers.

How is crypto taxed in Ireland if I received an NFT as a gift?

Receiving an NFT as a gift may trigger Capital Acquisitions Tax for you as the recipient if the value exceeds your available group threshold. When you later dispose of the gifted NFT, CGT applies to the gain from the date of acquisition, using the market value at the time you received it as your cost basis.

Are NFT royalties taxable in Ireland?

Yes. Royalties paid to you as the original creator of an NFT each time it resells on the secondary market are income, not capital gains. You must declare them in your annual tax return as income in the year you receive them, and they are subject to income tax, PRSI, and USC as applicable.

How is crypto taxed in India compared to Ireland?

India applies a flat tax to gains on virtual digital assets with no ability to offset losses across different assets, which differs significantly from Ireland's CGT framework. In Ireland, losses on one cryptoasset disposal can be offset against gains on another within the same class. Tax residency determines which country's rules apply to you, so if you have recently moved between the two countries, your residency position matters enormously.

What records do I need to keep for my NFT tax return?

For each NFT transaction, keep the date, the amount paid or received, the currency used, the fair market value in EUR at the time if the transaction involved another cryptoasset, any gas fees paid, and the marketplace or wallet involved. Revenue can request records going back several years, so maintaining a full transaction log from the outset is important rather than trying to reconstruct it at filing time.

Does crypto tax in the UK affect me if I moved to Ireland from the UK?

Your tax residency position determines which authority has the primary claim on your gains. If you are now tax resident in Ireland, Revenue is the relevant authority for your ongoing NFT activity. However, gains realised while you were UK-resident may have been subject to HMRC rules. If you have recently relocated, getting clarity on your residency status and any split-year treatment is worth doing before you file in either jurisdiction.

Can NFT losses reduce my tax bill in Ireland?

Yes, within the capital gains framework. If you dispose of an NFT at a loss, that loss can be offset against other chargeable gains in the same tax year, including gains from other cryptoasset disposals. If your losses exceed your gains in a given year, the excess can be carried forward to future tax years. Losses cannot be set against income from trading or employment.

What happens if I do not declare NFT gains to Revenue?

Revenue has the power to raise assessments, charge interest on underpaid tax, and apply penalties for non-disclosure or negligent filings. Blockchain data is increasingly accessible to tax authorities, and Revenue participates in international information-sharing frameworks. The risk of non-disclosure is real and growing, making accurate, timely filing the only sensible approach.

Source: CryptaTax