Do Wallet-to-Wallet Transfers Trigger Tax? A Crypto Tax Calculator Breakdown

One of the most common questions people ask when they first use a crypto tax calculator is whether moving coins between their own wallets creates a tax liability. The short answer is no, not in most jurisdictions. Moving bitcoin from your Coinbase account to your Ledger hardware wallet is not a disposal. You still own the same asset; you have simply stored it differently. However, the longer answer comes with important caveats around record-keeping, cost basis tracking, and the specific rules that apply where you live. Get those details wrong and your crypto tax report could show a phantom gain that was never real.

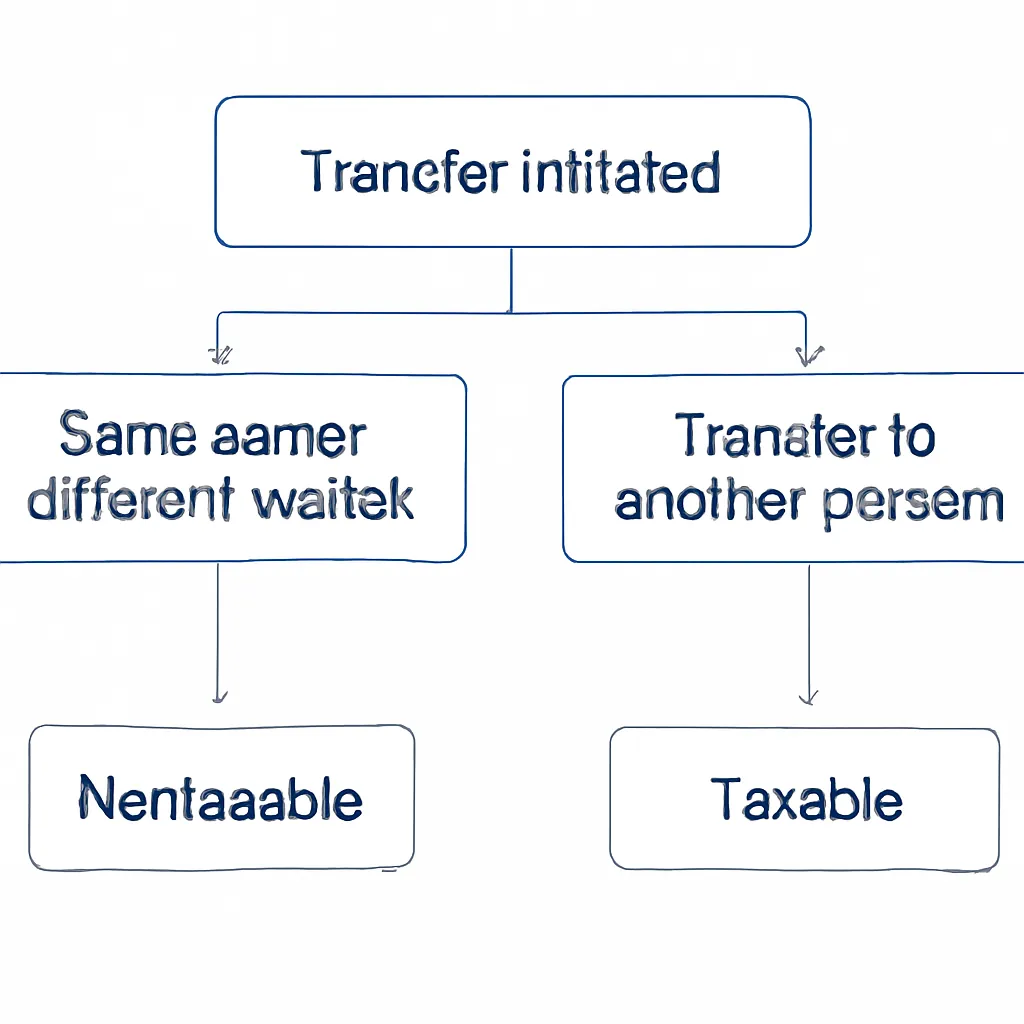

What Makes a Crypto Transaction Taxable?

Tax authorities in the US, UK, Australia, and most of Europe define a taxable disposal as an event where you give up beneficial ownership of a crypto asset in exchange for something else. That something else could be fiat currency, a different token, a good, or a service. The key question is always: did you stop owning the asset? When you send ETH from one wallet you control to another wallet you also control, the beneficial owner does not change. You remain the owner throughout. No disposal occurs, and no capital gains calculation is triggered at that point.

Defining a Taxable Disposal

Where people run into trouble is when they cannot prove that both wallets belong to them. If you send funds to an address you cannot link back to yourself in your records, your crypto tax software may flag it as an outgoing transfer with no corresponding incoming transaction on the same account. That gap can look like a sale to an automated system, and it can also look like an undisclosed transfer to a tax authority reviewing your files. Keeping clean records of every wallet address you own is not optional; it is the foundation of an accurate crypto tax report.

The Cost Basis Problem with Wallet Transfers

Even though a wallet-to-wallet transfer does not trigger tax, it can create serious problems when you eventually do sell or swap those assets. The issue is cost basis. When you move coins between wallets, the original acquisition cost must travel with those coins. If your crypto tax calculator loses track of when you first bought an asset and at what price, it will either assume a zero cost basis, which inflates your gain significantly, or it will fail to match the transaction at all, leaving an unresolved entry in your ledger.

Cost Basis Across Jurisdictions

Different countries handle cost basis assignment differently. The UK uses share pooling, where all units of the same coin are averaged together across wallets. The US allows specific identification methods such as FIFO, LIFO, or HIFO, but you must elect and consistently apply your chosen method. Australia generally defaults to FIFO. When you use a crypto capital gains calculator, it needs to know which method applies to you and it needs complete transaction history from every wallet you have ever used, otherwise the figures it produces will be wrong. A single missing wallet import can corrupt the entire calculation chain.

How Crypto Tax Software Handles Wallet Transfers

Good crypto tax software automatically detects wallet-to-wallet transfers and marks them as non-taxable internal movements. It does this by matching outgoing and incoming transactions of the same amount across wallets you have connected, within a reasonable time window to account for network confirmation delays. When the software finds a match, it tags the pair as a transfer, carries the original cost basis forward to the receiving wallet, and excludes the event from your gain and loss calculations.

Automatic Transfer Detection

The process sounds straightforward, but it depends entirely on you having imported all your wallets and exchange accounts. If you connected your Binance account but forgot about an old MetaMask wallet you used two years ago, any coins that passed through that wallet will appear as unmatched. The software cannot match what it cannot see. This is one of the most common reasons a crypto tax report shows figures that feel wrong: not because the tax rules are being applied incorrectly, but because the underlying data is incomplete.

Manual Tagging as Fallback

Most platforms allow you to tag transactions manually if the automatic matching fails. You can label a transfer pair yourself, assign the correct cost basis, and reprocess your calculations. It takes time, but it is far better than filing a return with phantom gains baked in.

When a Wallet Transfer Does Become Taxable

There are specific circumstances where what looks like a wallet transfer does create a taxable event. You need to understand these before assuming every internal move is clean.

Gifts to Others Are Taxable

Sending crypto to another person's wallet is the obvious one. Even if no money changes hands, gifting crypto is treated as a disposal at market value in many jurisdictions, including the UK and Australia. The US has gift tax rules that apply above certain thresholds. If you send coins to a family member, a business partner, or anyone else, that is not an internal transfer regardless of what you call it.

Wrapping and Bridging Risks

Wrapping tokens is another area to watch. Converting ETH to WETH, for example, may be treated as a swap between two distinct assets in some jurisdictions rather than an internal movement, because the token contract changes. The tax treatment of wrapped tokens is still unsettled in several countries, so checking the current position in your jurisdiction before you calculate crypto taxes on these transactions is sensible.

Bridging assets across blockchains can also trigger questions. Sending USDC from Ethereum to Arbitrum via a bridge involves burning one token and minting another. Whether that constitutes a disposal depends on how your local authority views the two representations of the asset. Some practitioners argue it does not, others treat it with caution. Until clear guidance exists, documenting the economics carefully is the safest approach.

Record-Keeping Rules That Apply Globally

Regardless of whether your transfers are taxable, you are required to keep records of all your crypto transactions in every major jurisdiction. The US requires records to support your cost basis claims for every asset. The UK requires records for at least six years from the filing date. Australia's ATO expects records to be kept for five years from the date of the relevant transaction. These are not soft suggestions; failing to keep adequate records can result in penalties even if your underlying tax position is correct.

Required Records for Transfers

For wallet transfers specifically, the records you need include the date of the transfer, the wallet addresses involved, confirmation that both addresses belong to you, the amount transferred, and the value at the time if you want to document that no disposal occurred. Screenshots, exchange statements, and blockchain explorer links all count as evidence. Storing these alongside your crypto tax report ensures you can respond to any query without scrambling for information after the fact.

The following table summarises the record-keeping obligations and general treatment of wallet-to-wallet transfers across four key jurisdictions.

Jurisdiction Summary Table

| Jurisdiction | Wallet-to-Wallet Transfer: Taxable? | Record-Keeping Period | Cost Basis Method |

|---|---|---|---|

| United States | No (same owner) | Indefinitely recommended; at least 3-7 years | FIFO, LIFO, HIFO (specific ID) |

| United Kingdom | No (same owner) | 6 years from filing date | Share pooling (Section 104) |

| Australia | No (same owner) | 5 years from transaction date | FIFO (default) |

| Germany | No (same owner) | 10 years | FIFO |

Network Fees on Transfers: Are They Deductible?

When you move crypto between wallets, you usually pay a network fee in the native token of that blockchain. Whether that fee is tax-deductible depends on the context. In the US, transaction costs that are directly related to an acquisition or disposal can typically be added to your cost basis or deducted from proceeds. A fee paid on an internal transfer that does not constitute a disposal sits in a grey area, and guidance is not definitive. In the UK, HMRC allows certain allowable costs to be deducted when calculating a gain, but only costs that are wholly and exclusively for the purpose of the acquisition or disposal.

Network Fee Deductibility

The practical takeaway is that network fees on pure wallet-to-wallet transfers are unlikely to generate a meaningful deduction in most cases, but they should still be recorded. If you later sell the assets that were transferred, your crypto capital gains calculator needs the full cost history, and fees can be part of that history depending on how your jurisdiction treats them. Ignoring fees entirely means you may be overpaying tax on eventual disposals.

Fee Treatment by Type Table

| Fee Type | Likely Tax Treatment (US) | Likely Tax Treatment (UK) | Record It? |

|---|---|---|---|

| Fee on purchase | Added to cost basis | Allowable acquisition cost | Yes |

| Fee on sale | Deducted from proceeds | Allowable disposal cost | Yes |

| Fee on internal wallet transfer | Unclear; conservative approach: record only | Generally not deductible | Yes |

| Fee on token swap | Part of disposal calculation | Part of disposal calculation | Yes |

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Jennifer is a freelance designer based in California who has been accumulating bitcoin since 2021 across three different platforms: a major US exchange, a non-custodial mobile wallet, and a hardware wallet she uses for long-term storage. In early 2024 she decides to consolidate everything onto the hardware wallet before filing her taxes. She moves funds from both the exchange and the mobile wallet across, paying small network fees on each transfer.

When Jennifer opens CryptaTax to prepare her crypto tax report, she imports all three wallets. The software automatically matches the outgoing transfers from her exchange and mobile wallet to the incoming transactions on her hardware wallet and tags them as internal movements. No capital gain is recorded. However, Jennifer notices that one transfer from 2022 did not match automatically because she had slightly rounded the amount when recording it manually at the time. She uses the manual tagging feature to link the two sides of that transfer, confirms the original cost basis carries forward, and reprocesses. Her final crypto capital gains calculator output reflects only her actual disposals, and the internal moves are cleanly excluded. She files with confidence knowing the figures are accurate.

Frequently Asked Questions

Does moving crypto between my own wallets count as a taxable event?

In most major jurisdictions, including the US, UK, Australia, and Germany, moving crypto between wallets you own and control is not a taxable disposal. No capital gain or loss is triggered because beneficial ownership has not changed. You should still record the transfer and ensure your cost basis carries across correctly.

How does a crypto tax calculator know a transfer is internal?

Crypto tax software matches outgoing and incoming transactions of the same amount across wallets you have connected, using timestamps and amounts to identify pairs. When it finds a match, it tags the event as a non-taxable internal transfer. If a wallet is missing from your import, the software cannot make that match and may treat the movement as an unexplained outflow.

What happens if I forget to import one of my wallets?

Missing wallet data is one of the most common causes of inflated gain figures in a crypto tax report. Outgoing transfers from wallets you have imported will appear as unsettled disposals, and incoming transfers on the missing wallet will never be recorded. Always audit your full wallet and exchange history before running your crypto capital gains calculator.

Are network fees on internal transfers tax deductible?

The deductibility of fees on internal transfers is unsettled in most jurisdictions. In the US and UK, fees are generally deductible only when directly connected to an acquisition or disposal. A fee on a purely internal move is unlikely to qualify, but you should still record it in case guidance changes or it becomes relevant to a later disposal calculation.

Is sending crypto to a family member a wallet-to-wallet transfer?

No. Sending crypto to someone else, including a family member, is a disposal or a gift, not an internal transfer. In the UK and Australia this triggers a capital gains event at market value. In the US it may trigger gift tax obligations above certain thresholds. Record the fair market value at the time of transfer and include it in your tax calculations.

Does wrapping a token, such as ETH to WETH, trigger tax?

The tax treatment of token wrapping is unsettled and varies by jurisdiction. Some tax authorities may treat the exchange of ETH for WETH as a swap between two distinct assets, which would constitute a disposal. Others take the view that the economic substance has not changed. If you use a crypto tax calculator, check how it categorises wrap transactions and review the current guidance in your country.

How do I file crypto taxes if I have dozens of wallets?

The practical answer is to use crypto tax software that supports bulk wallet imports via API connections or CSV uploads. Connect every wallet and exchange account you have ever used, let the software match internal transfers automatically, then review and manually resolve any unmatched transactions before generating your final crypto tax report. Trying to reconcile dozens of wallets manually in a spreadsheet is error-prone and time-consuming.

What records do I need to keep for wallet-to-wallet transfers?

Keep a record of the date, the sending and receiving wallet addresses, confirmation that both addresses belong to you, and the amount transferred. Blockchain explorer links or exchange withdrawal statements work well as evidence. These records support your position that no disposal occurred and ensure your cost basis tracking remains accurate when you eventually calculate crypto taxes on the assets involved.

Can the tax authority see my wallet transfers?

Blockchain transactions are publicly visible on-chain, and tax authorities in the US, UK, and EU have access to chain-analysis tools that can trace movements between addresses. Exchanges operating in these jurisdictions are also required to report user data under frameworks such as CARF and 1099-DA. Assuming transfers are invisible is not a reliable strategy; accurate reporting and clean records are.

Does the cost basis change when I transfer crypto between wallets?

No. The original acquisition cost of an asset should carry across unchanged when you make an internal transfer. Your crypto tax software should handle this automatically if all wallets are imported. If you are tracking manually, make sure you record the original purchase date and price alongside the asset as it moves between addresses, because those figures determine your gain or loss when you eventually dispose of it.

Source: CryptaTax