Crypto Mining Tax: What Every Individual Needs to Know

Crypto mining tax is one of the most misunderstood areas of personal tax. Many miners assume that because they are not selling anything, they have no immediate liability. That assumption is wrong in most major jurisdictions. When you successfully mine a block and receive a reward, tax authorities in the US, UK, Australia, Canada, and elsewhere treat that reward as taxable income at the moment you receive it. Then, when you eventually sell or exchange those coins, a second tax event is triggered. Two taxes, one transaction history. Understanding how both layers work is the starting point for getting your return right.

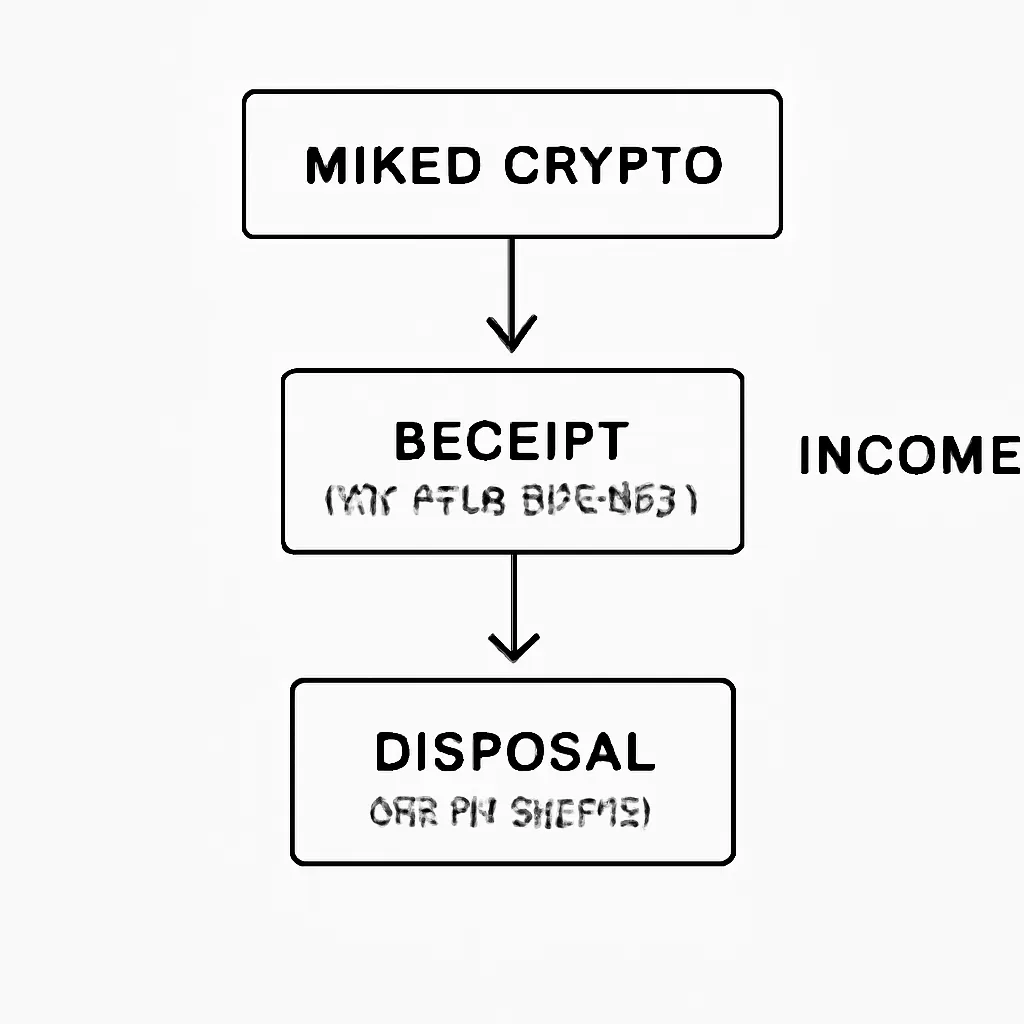

How Crypto Mining Tax Works: The Two-Stage Liability

Most tax authorities split the crypto mining tax picture into two distinct stages, and conflating them is one of the most common mistakes individual miners make.

Income Tax on Receipt

The first stage is income tax. When mined coins land in your wallet, their fair market value at that exact moment is treated as ordinary income. If you mined one bitcoin on a day when it was trading at a certain price, the full value of that bitcoin is added to your taxable income for that year. You owe income tax on it regardless of whether you sell it, hold it, or lose access to the wallet. The receipt itself is the taxable event.

The second stage is capital gains tax. Your income tax value becomes your cost basis. If you later sell, swap, or spend those coins, you calculate a gain or loss against that basis. A rise in value between receipt and disposal is a taxable capital gain. A fall is a capital loss, which may be usable to offset other gains depending on your jurisdiction's rules.

The table below summarises how the two stages interact.

Two-Stage Summary Table

| Stage | Triggering Event | Tax Type | Basis for Calculation |

|---|---|---|---|

| 1 | Receiving mined coins | Income tax | Fair market value at date of receipt |

| 2 | Selling, swapping, or spending those coins | Capital gains tax | Disposal proceeds minus cost basis from Stage 1 |

Crypto Mining Tax Rules by Jurisdiction

The broad framework is consistent across major jurisdictions, but the rates, thresholds, and classifications differ enough to matter. Where you mine, and where you are tax-resident, determines which ruleset applies to you.

US Tax Rules for Miners

In the United States, the IRS treats mined cryptocurrency as ordinary income, taxed at your marginal rate. If you mine as a business, you may deduct eligible expenses such as electricity and hardware depreciation. If you mine as a hobby, your deduction options are far more limited under current rules.

In the United Kingdom, HMRC draws the same business versus hobbyist line. For most individuals, mined coins are subject to income tax and National Insurance on receipt. Disposal then falls under capital gains tax rules, with the annual exempt amount potentially reducing your liability. HMRC has published detailed cryptoassets guidance that addresses mining specifically.

In Australia, the Australian Taxation Office treats mined crypto as ordinary income at the market value on the day of receipt. Holding coins for more than twelve months before disposal may qualify you for the capital gains tax discount that applies to individuals.

Canada follows a similar pattern. The Canada Revenue Agency treats mining proceeds as business income for most active miners, making expenses potentially deductible.

Jurisdiction Comparison Table

| Jurisdiction | Income Tax on Receipt | Capital Gains on Disposal | Expense Deductions Available |

|---|---|---|---|

| United States | Yes, at marginal rate | Yes | Yes, if business activity |

| United Kingdom | Yes, income tax and NI | Yes | Yes, if trade activity |

| Australia | Yes, at marginal rate | Yes, CGT discount if held 12+ months | Yes, if business activity |

| Canada | Yes, as business income | Yes | Yes, if business activity |

Crypto Mining Tax Versus Crypto Staking Tax

Miners often ask how their obligations compare to those of stakers. Crypto staking tax and crypto mining tax share the same basic structure in most jurisdictions: rewards are taxable income on receipt, and disposal triggers a capital gain or loss. The key difference is technical rather than fiscal. Mining uses proof-of-work, consuming computational energy to validate transactions. Staking uses proof-of-stake, where validators lock up existing holdings to earn rewards.

Staking Tax Compared to Mining

Is staking taxable? Yes, in virtually every jurisdiction that has issued guidance. The UK, US, and Australia all treat staking rewards as taxable income when received. There is ongoing legal debate in the US about whether newly created tokens should be taxed at receipt or only at disposal, but until that debate produces binding guidance, most tax professionals advise treating them as income on receipt to stay compliant.

The practical difference for your records is that staking rewards tend to arrive in smaller, more frequent amounts, making automated tracking even more important. The income calculation method is the same: fair market value at the date and time of each reward receipt.

DeFi Tax, NFT Tax, and How Mining Fits the Bigger Picture

If you are a miner who also participates in broader on-chain activity, you are dealing with multiple overlapping tax obligations. Defi tax rules apply when you earn yield from liquidity pools, lending protocols, or automated strategies. How are defi rewards taxed? The short answer is: the same way mining rewards are. Most authorities treat DeFi income as ordinary income on receipt, with a subsequent capital gain or loss on disposal.

DeFi and NFT Tax Overlaps

NFT tax adds another dimension. Minting an NFT from mined coins, selling an NFT, or receiving royalties each carries its own tax event. Selling an NFT is generally treated as a disposal of a capital asset, so your gain is calculated against the cost of creating or acquiring it. If you used mined coins to pay minting fees, those coins were also disposed of at the point of payment.

Crypto trading tax layers on top of all of this. Every trade between cryptocurrencies is a taxable disposal in most jurisdictions, including swapping mined coins for another token. The combined picture can become complex quickly, particularly for anyone who mines, stakes, provides liquidity, and trades within the same tax year.

Record-Keeping: The Foundation of Every Compliant Return

Tax authorities increasingly have access to blockchain data and exchange reporting. Trying to reconstruct records at filing time from memory is not a strategy. Every serious miner needs a systematic approach to documentation from day one.

Required Records for Miners

The records you need to keep include the date and time of each mined reward, the amount received in the relevant cryptocurrency, the fair market value in your local fiat currency at the moment of receipt, the source wallet address, and any transaction fees paid. For disposals, you need the date, the proceeds in fiat, the cost basis tied back to the original receipt, and the resulting gain or loss.

How long to keep records varies by jurisdiction. The IRS generally expects at least three years from the filing date, but longer periods apply in certain circumstances. HMRC expects records for at least five years after the relevant Self Assessment deadline. The ATO advises keeping records for five years from the date you lodge your return.

Record Retention Periods Table

| Jurisdiction | Minimum Record Retention Period | Key Authority |

|---|---|---|

| United States | At least 3 years from filing date | IRS |

| United Kingdom | At least 5 years after Self Assessment deadline | HMRC |

| Australia | 5 years from date of lodgement | ATO |

| Canada | 6 years from end of the tax year | CRA |

Common Mistakes That Trigger Investigations

Most crypto tax problems stem from a small number of repeated errors. The first is ignoring income tax on receipt and only reporting gains at the point of sale. This understates income in the year of mining and may trigger penalties for underpayment.

Ignoring Income Tax on Receipt

The second common error is using the wrong cost basis. If you received mined coins and later sold them, your basis is the fair market value on the day you received them, not zero. Using a zero basis inflates your capital gain and leads to overpayment, or misreporting if the return is later reviewed.

The third mistake is failing to report small or frequent rewards. Staking and DeFi rewards that arrive daily in small amounts can add up to a meaningful annual income figure. Tax authorities do not offer a de minimis exemption for crypto income in most jurisdictions, even if individual transactions are tiny.

Failing to Report Small Rewards

The fourth error is treating crypto trading tax differently from mining tax within the same return. All taxable events need to be reported together, with consistent cost basis methodology applied across the entire portfolio.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Priya is a software developer based in the UK who began mining Ethereum Classic as a side activity. She set up a small rig at home and received mining rewards at irregular intervals throughout the tax year. At the end of the year, she assumed she only needed to report any gains when she eventually sold her coins.

When Priya started using CryptaTax to organise her records, she discovered that each mining reward had already created an income tax liability at the point of receipt. Her total annual mining income, calculated by aggregating the sterling value of each reward on the day it was received, was higher than she expected. She also realised that a batch of coins she had sold for a profit had a cost basis equal to the income value she had already reported, not zero.

CryptaTax calculated her income tax position from the mining receipts, set her correct cost basis for each lot, and produced a capital gains summary for the coins she had sold. Priya filed her Self Assessment with accurate figures for both layers of liability, avoiding the penalties that would have come from the original underreporting.

Frequently Asked Questions

Is crypto mining taxable income?

Yes, in virtually all major jurisdictions including the US, UK, Australia, and Canada. When you receive mined coins, the fair market value at the moment of receipt is treated as taxable income. You owe income tax on that value regardless of whether you sell the coins afterward.

When does crypto mining tax apply, at receipt or at sale?

Both. Income tax applies at the point of receipt, based on the fair market value of the coins on that day. Capital gains tax then applies when you later sell, swap, or spend those coins, calculated against the basis you established at receipt.

Can I deduct electricity and hardware costs from my mining income?

In most jurisdictions, deductions are available if your mining activity qualifies as a business or trade rather than a hobby. The distinction depends on factors like the scale of your activity, profit intent, and regularity. If HMRC, the IRS, or the ATO classifies your activity as a hobby, deduction options are significantly restricted.

Is crypto staking taxable in the same way as mining?

Yes, broadly. Crypto staking tax follows the same two-stage structure in the UK, US, and Australia: rewards are income on receipt, and disposal creates a capital gain or loss. The technical mechanism differs from mining, but the tax treatment is closely aligned in most jurisdictions that have issued guidance.

How are DeFi rewards taxed compared to mining rewards?

How DeFi rewards are taxed follows a similar pattern to mining. Most authorities treat DeFi income as ordinary income at the point of receipt, based on fair market value. A subsequent disposal of those tokens is then treated as a capital event. The complexity increases when DeFi protocols involve multiple wrapped or synthetic assets.

Do I need to report every small mining reward, even tiny amounts?

Yes. Most jurisdictions do not provide a de minimis exemption for crypto income, meaning every reward must be reported regardless of size. Frequent small rewards from staking or DeFi protocols accumulate over a year and can represent material income. Automated tracking tools help capture every event without manual effort.

What records do I need to keep for crypto mining tax purposes?

You need the date and time of each reward, the amount received, the fair market value in your local currency at that moment, the wallet address, and any transaction fees. For subsequent disposals, you need the date, proceeds, and the original cost basis. Retention periods vary by jurisdiction, ranging from three to six years.

Does crypto trading tax work differently from mining tax on the same return?

The taxes interact but follow different rules at the point of triggering. Crypto trading tax arises when you dispose of any cryptoasset, including coins you mined. The gain is calculated against your cost basis, which for mined coins is the income value you reported at receipt. Both must be reported consistently using the same cost basis methodology throughout your return.

Is NFT tax relevant for crypto miners?

Yes, if you use mined coins to mint NFTs, pay gas fees, or trade NFTs. Each use of mined coins is a disposal, triggering capital gains tax on any gain since receipt. Selling an NFT is itself a disposal of a capital asset. Miners who are also active in NFT markets face multiple overlapping taxable events within the same portfolio.

What happens if I fail to report mining income?

Tax authorities in the US, UK, Australia, and Canada have increased access to blockchain data and exchange reporting. Failing to report mining income can result in penalties, interest on underpaid tax, and in serious cases, investigation. Filing an amended return voluntarily before an authority contacts you typically results in lower penalties than a prompted correction.

Source: CryptaTax